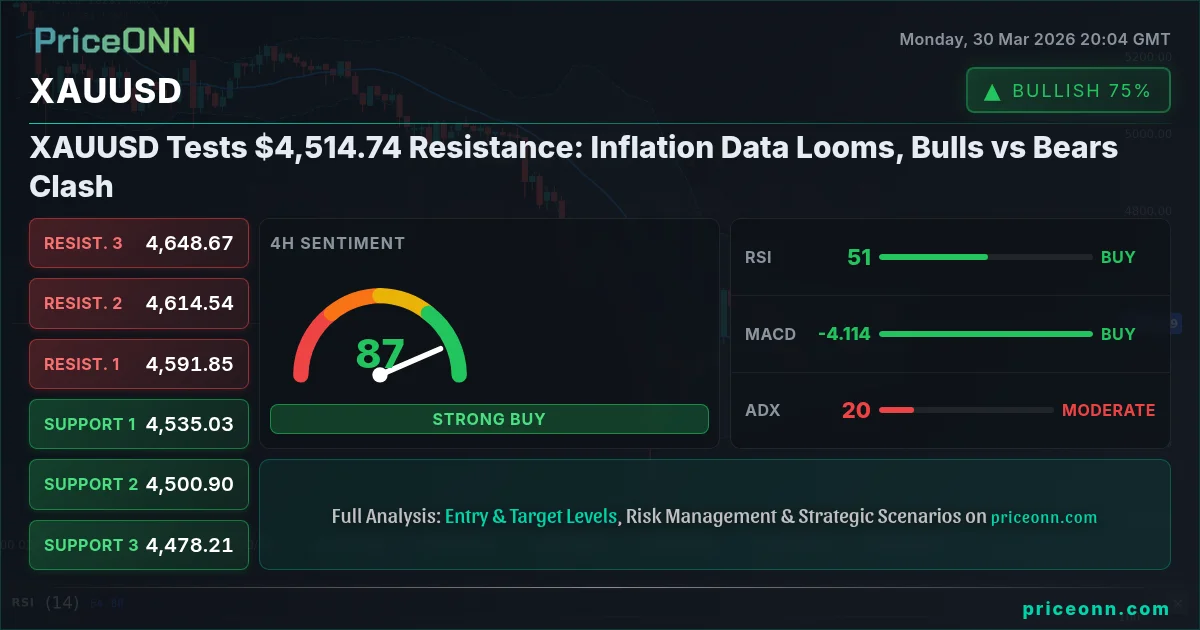

Gold Ticks Higher Ahead Of Powell's Speech

Markets Brace for Uncertainty as Gold Finds Safe Haven

The precious metal staged a notable recovery, reversing earlier declines to trade comfortably above the $4,500 per ounce level this Monday. This upward momentum for gold unfolded against a backdrop of conflicting signals emanating from both Iran and the United States regarding the status of de-escalation efforts. Spot gold registered a gain of 0.8 percent, reaching $4,531 an ounce, while U.S. gold futures for June delivery mirrored this trend, climbing 0.8 percent to settle at $4,560.

Adding to the complex market sentiment, the U.S. dollar hovered near a ten-month peak. It was on track for its most substantial monthly appreciation since July of the previous year. This strength in the dollar is largely attributed to heightened energy risks fueled by intensifying U.S.-Iran diplomatic and military posturing, which has unsettled global investor confidence.

The ripple effects of this geopolitical friction were dramatically evident in the energy markets. Crude oil prices were poised for their largest monthly gain on record as the Middle East conflict entered its fifth week without any definitive resolution on the horizon. The situation remains fluid, with significant implications for global supply chains and inflation expectations.

Conflicting Signals from Washington and Tehran

Adding a layer of intrigue, U.S. President Donald Trump offered a seemingly conciliatory note, describing Iran's interim leadership as "very reasonable." This statement briefly ignited hopes for a potential diplomatic breakthrough. However, these optimistic undertones were quickly juxtaposed with fresh, more aggressive rhetoric from the President, who expressed a desire to "take the oil in Iran" and suggested the U.S. could readily seize Kharg Island, Iran's critical oil export hub.

The market is now bracing for the possibility of a protracted conflict in the Gulf region. The recent involvement of the Houthi movement in the escalating Iran war, coupled with the deployment of additional U.S. military assets to the Middle East, has heightened concerns. Reports suggest the Pentagon is preparing for potentially weeks of ground operations within Iran.

Fears are also mounting that Houthi forces, emboldened by the regional instability, may target commercial vessels traversing the vital Red Sea shipping lanes. Furthermore, key energy infrastructure within Saudi Arabia could also become a focal point for such attacks, potentially disrupting global energy supplies even further.

Economic Calendar and Fed Watch

Looking ahead, the economic calendar presents a crucial week for market direction. Investors will be closely monitoring key U.S. data releases. These include the JOLTS job openings report, consumer confidence figures, the ADP employment survey, the final readings for S&P manufacturing and services Purchasing Managers' Indexes, and the highly anticipated March jobs report. Each of these indicators will offer vital clues about the health of the U.S. economy.

Market participants are also keenly focused on scheduled speeches from influential Federal Reserve officials. Fed Chair Jerome Powell and New York Fed President John Williams are set to deliver remarks later today. Their commentary will be scrutinized for any hints regarding potential shifts in U.S. monetary policy. Philadelphia Fed President Anna Paulson acknowledged that the Iran conflict introduces new risks to both inflation and economic growth, though she refrained from specifying immediate policy implications.

The prevailing sentiment in the markets, as reflected by CME's FedWatch Tool, indicates that traders are currently not pricing in any interest rate cuts from the U.S. Federal Reserve this year. This stance marks a significant shift from expectations of two rate cuts that were prevalent before the recent escalation of Middle East tensions.

Market Ripple Effects

The current geopolitical climate, marked by U.S.-Iran tensions and rising oil prices, creates a complex environment for traders. Gold's role as a traditional safe-haven asset is being amplified, suggesting continued upward potential as long as uncertainty prevails. The U.S. dollar's strength, driven by risk aversion, could put pressure on emerging market currencies and potentially impact U.S. export competitiveness.

Traders should closely monitor the price action in crude oil (Brent and WTI), as further escalation could lead to significant price spikes, feeding into inflation expectations and potentially influencing central bank decisions globally. The USD/CAD currency pair is also a key watch, given Canada's status as a major oil producer; a sustained rise in oil prices could offer support to the Canadian dollar against its U.S. counterpart.

Furthermore, the heightened risk appetite globally, potentially triggered by prolonged conflict, could affect equity markets. While defensive sectors might see inflows, broader market sentiment could turn cautious. Investors should also keep an eye on bond yields, as inflation expectations could begin to creep higher, potentially impacting fixed-income strategies. The focus on Fed officials' speeches underscores the delicate balance between managing inflation risks and supporting economic growth, making any hawkish or dovish signals particularly impactful for interest-rate sensitive assets.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join Channel