Solid Labour Report May Put Growing Inflation Risks Even More in the Spotlight

Bond Market Turmoil and ECB Expectations

Core bond markets experienced a brief respite before renewed selling pressure emerged. German Bunds significantly underperformed U.S. Treasuries, with substantial offloading driving net daily yield increases between +2.9 bps (30-year) and +11.7 bps (5-year) in a bear flattening scenario. Market focus shifted to short-dated bonds amidst growing expectations for interest rate hikes by the European Central Bank (ECB). The implied probability of a rate increase by the end of the year surged to 65%, even reaching 75% at one point, compared to a 55% chance of a rate cut just a week prior, before the escalation of tensions in Iran.

Recent ECB meeting minutes indicated the central bank's readiness to respond to evolving economic conditions in either direction. This stance followed warnings from ECB Vice President de Guindos, as well as Rehn (Finland) and Nagel (Germany), suggesting that a prolonged conflict in Iran could exacerbate inflationary pressures. ECB policymakers appear to have learned valuable lessons from the 2022 Ukraine war, during which they initially dismissed the energy-driven price surge as transitory. While this assessment might have held true in an era of structurally low inflation, the current landscape has undergone a significant transformation.

Oil Price Volatility and Geopolitical Risks

Oil prices experienced considerable volatility, fluctuating in response to conflicting reports regarding Iran's nuclear program and its stance on the Strait of Hormuz. Despite initial reports suggesting a willingness to curtail uranium enrichment, subsequent news indicated near-total disruption of shipping traffic in this crucial oil supply artery. The prevailing geopolitical climate strongly suggests that oil prices will remain elevated as long as regional tensions persist. Brent crude surpassed the $85 per barrel mark, reaching levels not seen since mid-2024. Dutch TTF gas futures initially surged by 12% before settling at a 4% gain, trading above €50/Mwh.

The prospect of another energy crisis, following the economic challenges of 2022, has dampened the appeal of European assets. Stock markets experienced a downturn, with the EuroStoxx50 falling by 1.5%. The euro weakened, but losses were contained, with EUR/USD trading around the 1.16+ level.

US Economic Outlook and Policy Signals

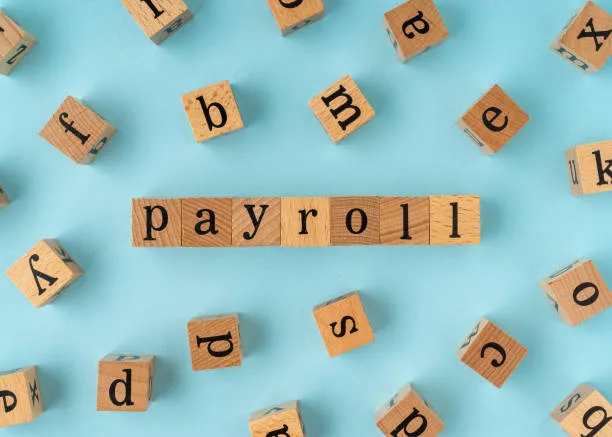

U.S. yields trended upward, albeit at a slower pace than their European counterparts. The yield curve shifted higher by 1.8-4.5 bps, with the intermediate part of the curve underperforming the extremes. The latest payroll data has the potential to further bolster this week's recovery. Federal Reserve Governor Bowman noted emerging evidence of labor market stabilization, signaling a preference for maintaining the current interest rate stance. Numerous other Fed policymakers are scheduled to share their perspectives before the communication blackout period commences this weekend.

A robust labor market report could intensify focus on escalating inflation risks, potentially overshadowing concerns about downside employment risks. The anticipation of interest rate cuts may be pushed further into the future, with markets now pricing in less than two full rate cuts for the entirety of 2026. This backdrop supports a bullish outlook for the U.S. dollar as the week concludes.

Policy Shifts and Central Bank Actions

The U.S. Office of Foreign Assets Control (OFAC) issued a temporary license allowing Indian refiners to purchase Russian oil loaded on or before March 5, expiring on April 4. Treasury Secretary Scott Bessent characterized this measure as a short-term effort to maintain global oil flows, asserting that the transactions would not significantly benefit the Russian government and only involve oil already in transit. This move represents a notable policy shift from the U.S., which had previously pressured India to reduce its Russian oil purchases due to the war in Ukraine.

In Poland, National Bank of Poland (NBP) policymaker Henryk Wnorowski indicated that further rate cuts will be avoided until the conflict in Iran is resolved. Wnorowski suggested that the likelihood of the policy rate reaching 3.25%/3.5% has diminished considerably. These comments followed the NBP's decision to cut the policy rate by 25 bps to 3.75%, based on projections indicating that inflation would remain near the 2.5% target through 2028. Despite the rate cut, the Polish 2-year swap rate rose by 7 bps to 3.80%, after sharp increases earlier in the week. The zloty has weakened from levels near EUR/PLN 4.2175 to around EUR/PLN 4.2725.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join Channel