The Billion-Dollar Debt Deals Exposing an Oil Giant

A Torrent of Capital Masks Underlying Weaknesses

Angola's national oil company, Sociedade Nacional de Combustíveis de Angola, or Sonangol, has recently pulled in substantial financial backing, totaling $2.65 billion. This massive influx of capital, primarily from a syndicate of international financial institutions including Société Générale, First Abu Dhabi Bank, Standard Bank of South Africa, and Absa, is earmarked for critical operating expenses and future capital investments. Local Angolan banks also contributed, adding $105 million to the pot through institutions like Banco Fomento de Angola (BFA), Banco Millennium Atlântico, and Banco Angolano de Investimentos (BAI).

This latest financial maneuver is not an isolated event. Since the year began, Sonangol has been actively restructuring its financial landscape. In January alone, the company secured a $1.75 billion facility from the African Export-Import Bank (Afreximbank), intended to bolster its working capital and crude trading activities. Almost simultaneously, Sonangol successfully raised $750 million in the international markets via a five-year bond, offering a 10% coupon to investors.

The company's financial quest continues, as it is currently in discussions seeking an additional $4.8 billion from Chinese and European financiers. This capital is crucial for bridging a funding gap for the ambitious $6.6-billion Lobito Refinery project. Yet, beneath the surface of these substantial capital raises, a more complex and concerning picture of Angola's oil model emerges.

Examining Sonangol's Profitability Puzzle

While the large-scale financing from global banks might suggest robust operational health, it paradoxically highlights significant vulnerabilities. The core issue appears to be a struggle for profitability, coupled with a broad, and perhaps ill-advised, diversification into non-essential business sectors, and a noticeable decline in production levels. These factors are collectively placing immense pressure on the nation's flagship energy enterprise.

Sonangol's primary Oil & Gas operations are finding it difficult to generate substantial profits. For the 2025 financial year, the company reported an overall net profit of 862.4 billion Kwanza (approximately $940 million). However, a closer inspection of its upstream exploration and production (E&P) segment reveals a far less impressive performance. This crucial division yielded a profit of only Kz97.1 billion ($105 million), despite generating a colossal Kz4 trillion ($4.36 billion) in revenue. The slim profit margin is attributed to exceptionally high operational costs, significant asset depreciation, and substantial tax liabilities.

The downstream refining and distribution segment fared even worse, posting a staggering loss of Kz820.3 billion ($895 million) within the same fiscal year. The numbers tell a clear story: a significant portion of Sonangol's reported earnings, specifically 53% of its 2025 profits, did not originate from its core energy activities. Instead, these earnings stemmed from dividends received from external corporate holdings.

Diversification's Cost and Future Outlook

These external stakes include significant investments in Portugal's Galp Energia, Millennium BCP bank, and the Angola LNG project. Sonangol holds a substantial 22.8% stake in the Angola LNG facility, a $12-billion venture designed to process up to 1.1 billion cubic feet of natural gas daily and produce 5.2 million metric tons of liquefied natural gas annually. This project is vital for mitigating gas flaring from offshore oil fields, converting it into a valuable clean energy export.

Adding to Sonangol's financial strain, the company's internal cash reserves are alarmingly low, covering only an estimated 18% of its immediate financial obligations, according to a recent warning from the statutory audit board. This liquidity crunch is exacerbated by approximately Kz8.2 trillion ($8.96 billion) in outstanding amounts owed by third parties and the Angolan state itself.

Much of Sonangol's predicament can be traced back to years of systemic government influence, which saw the company function as an unofficial sovereign wealth fund. This led to the accumulation of stakes in around 65 non-core businesses, ranging from aviation services (Sonair) to medical facilities. These non-strategic holdings have proven to be a considerable financial drain, accumulating billions in losses over time. Consequently, poor cash flow management and delayed upstream investments have contributed to a steady decline in national crude output, which has fallen to approximately 1.1 million barrels per day from a peak of 2 million barrels per day in 2008. The remaining prospective oil acreage often requires substantial capital expenditure due to its ultra-deepwater location.

Strategic Shifts and Market Realignments

Despite these challenges, a path towards recovery is being forged. Sonangol is actively divesting more than 70 non-core subsidiary shareholdings across sectors like real estate, aviation, banking, and telecommunications to sharpen its focus on core energy operations. Concurrently, the company is undertaking a significant restructuring of its debt obligations to improve liquidity and is actively seeking partnerships with international energy majors, such as Chevron, for the development of new deep-water assets.

The Angolan government is also granting Sonangol greater operational autonomy. The recent transfer of regulatory and licensing authority from Sonangol to the National Oil, Gas and Biofuels Agency (ANPG) now allows Sonangol to compete on a more equal footing with international operators for oil blocks. The ultimate objective of this comprehensive restructuring effort is to prepare for a public offering, aiming to list up to 30% of Sonangol's shares on the stock market by 2027. The planned phased listing will commence on the Luanda Stock Exchange, with subsequent listings anticipated on major international exchanges in the U.S. and U.K.

Market Ripple Effects

This substantial financing and restructuring by Sonangol has several potential implications for related markets. The immediate impact is on Angola's sovereign credit profile, as such large debt deals can influence its credit ratings and borrowing costs. The stability and future production of Angolan crude oil, a significant global supply component, will be closely watched. This could affect benchmark crude oil prices, particularly Brent and WTI, if production levels deviate significantly from expectations.

Furthermore, the involvement of major international banks like Société Générale and Standard Bank suggests a degree of confidence in the Angolan energy sector's future, potentially influencing investment flows into African energy projects. The success of the Lobito Refinery project, should it secure its full funding, could also impact regional energy dynamics and fuel prices. The planned IPO for 2027 could also be a significant event for emerging market equities, particularly within the energy sector, attracting investor interest if the restructuring proves successful.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelOil prices tumbled as markets bet Strait of Hormuz disruptions will ease, with Brent down 10% on the week and Middle East crude benchmarks slipping into contango. Friday, June 26, 2026 Whilst ship transits through the Strait of Hormuz remain a fraction of their previous norm (130-140 transits per day), plunging crude oil prices suggest the commodity markets anticipate that flows would start to recover sooner than later. The two Middle Eastern crude benchmarks, Dubai and Murban, have flipped...

European officials are expected to visit Baghdad in the coming weeks for high-level talks on energy cooperation, just hours after Iraq warned it could leave OPEC unless the producer group grants the country a higher production quota. According to Iraqi sources cited by Shafaq News, the discussions will focus on expanding cooperation across Iraq's oil, gas and electricity sectors. Planned talks include projects to capture associated gas, increase power generation, expand energy storage capacity...

Saudi Arabia is expected to slash the official selling prices of its crude loading for Asia in August, as Middle East’s crude benchmarks crashed amid the tentative reopening of the Strait of Hormuz and the oil supply increase from the region. Saudi oil giant Aramco, the world’s single-biggest crude oil exporter, is expected to slash the OSP of its flagship Arab Light crude by between $6.50 and $8.00 per barrel, a of industry sources showed on Friday. Refiners polled by Reuters...

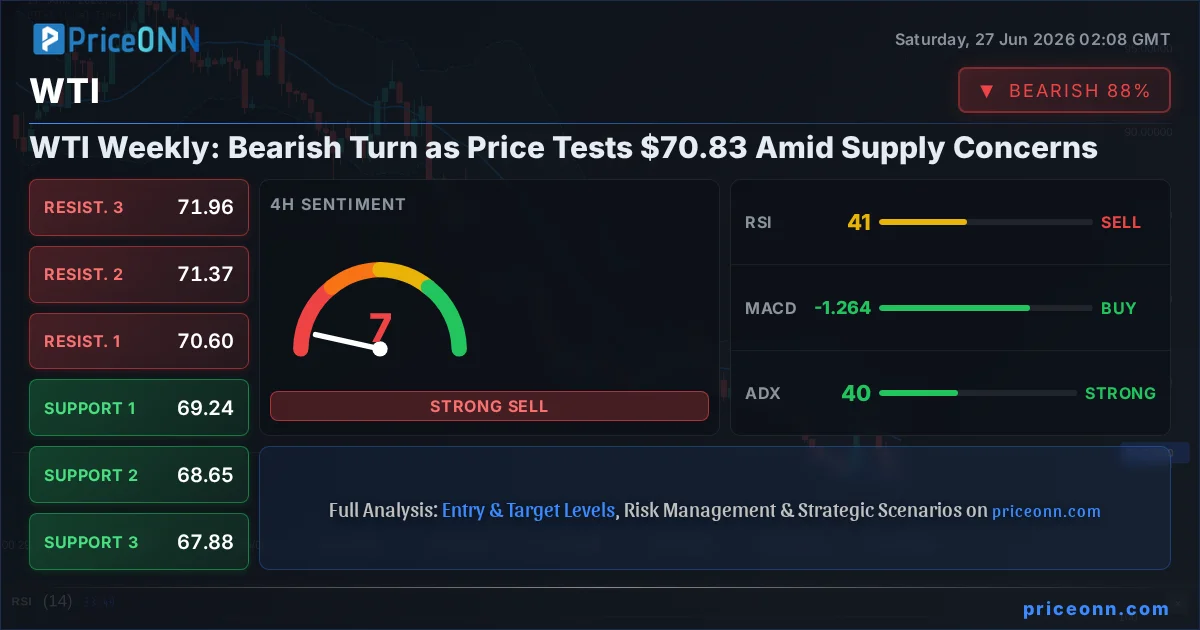

August WTI crude oil futures kept falling sharply during the week ending June 26. Traders continued to take out the extra price they had added earlier because they worried about possible supply problems in the Middle East. The contract moved between a high of $78.14 and a low of $68.90 before finishing at $71.53. That was down $3.99, or 5.28 percent, from the week before. The selling went on for most of the week. Traders stopped focusing as much on the chance of oil supplies getting cut off in...

Chinese crude oil imports this month are on course to book an even weaker month than May, according to Kpler data, which sees the daily average at just 6.4 million barrels, as cited by Bloomberg. Data from Vortexa suggests a similar daily import level, the publication added. This would be the weakest import rate since October 2016, Bloomberg noted, and an 8% decline on May volumes. Those averaged 7.82 million barrels, according to customs data, down by 29% on the year and 17% on April. The May...

Crude Oil prices edge lower on Friday, with the US benchmark West Texas Intermediate (WTI) barrel changing hands at $69.65 at the time of writing. This is the lowest price since February 27, one day before the US and Israel launched a joint attack on Iran.

Kazakh President Kassym-Jomart Tokayev’s visit to the EU’s headquarters in Brussels has yielded agreements and MoUs potentially valued at over 12 billion dollars. The key deal involves the purchase of 50 Airbus passenger jets for 7.1 billion euros. Tokayev’s visit, which concluded June 23, focused on developing Middle Corridor trade links within the context of the EU’s Global Gateway program. Prominent among Tokayev’s meetings in Brussels were discussions with European Commissioner for Trade...

Russia has emerged as one of the clearest commercial beneficiaries of the US-Israel war with Iran. Before March 2026, buying Russian crude was widely treated as a sanctions risk that only Chinese and, to a lesser extent, Indian private companies could comfortably absorb. The first US waiver for Russian barrels, announced on March 12, changed that calculation. It showed that, during a major Middle Eastern supply disruption, Asia could not balance its oil market without Russian crude, and even...

The Tennessee Valley Authority released its preliminary 2026 integrated resource plan on Monday, saying load growth in its footprint is already outpacing the reference case forecast in its draft IRP, and that it has incremental capacity needs for between 7 GW and 26 GW of natural gas between now and 2040. “TVA’s actual and forecasted electricity demand has increased relative to the draft IRP’s Reference scenario and is approaching the Higher Growth Economy scenario primarily due to data center...

ADNOC, the national oil company of Abu Dhabi, has cut the official selling price for July for its flagship Murban crude to $101.48 per barrel, down from $104.44 a barrel for June, amid weakening international and Middle Eastern benchmark oil prices. ADNOC’s recent pricing list for July, reported by Economy Middle East, reflects softening market conditions following the tentative reopening of the Strait of Hormuz. ADNOC has priced its other grades, Umm Lulu, Das, and Upper Zakum, at par with...

West Texas Intermediate (WTI) US Oil trades around $69.30 at the time of writing, down 0.65% on Thursday. The American benchmark Crude is now posting a fourth consecutive day of losses, weighed down by a convergence of supply-side factors reshaping market expectations.

The national oil company of the United Arab Emirates, ADNOC, has signed agreements with BP and TotalEnergies to let the European oil and gas supermajors take 10% each in the consortium developing one of Abu Dhabi’s largest gas fields. Both BP and TotalEnergies announced on Thursday they had signed their respective concession agreements to join the development of the Bab Gas Cap project in Abu Dhabi. BP will now hold a 10% interest in the Bab Gas Cap concession, which is expected to produce up...