Warsh: the New Fed Chief Would Like to Repeat Greenspan’s Trick of Ignoring a Productivity Boom

A Look Back at a Central Banking Legend

The financial world is reflecting on the passing of Alan Greenspan, a titan of central banking who led the Federal Reserve for two decades, steering the U.S. economy through a period of significant transformation at the turn of the millennium. Nominated multiple times by different presidents, Greenspan cemented the Fed's standing, securing a level of independence and public trust that remains influential. His tenure, however, is not without its critics, particularly concerning his approach to financial regulation, which some argue sowed the seeds for the 2008 financial crisis. Yet, a key aspect of his legacy offers a compelling parallel for today's economic discussions.

In the mid-1990s, Greenspan recognized a fundamental shift. He posited that the burgeoning internet was not merely a technological novelty but a genuine positive supply shock. This, he reasoned, would naturally suppress costs, dampen inflationary pressures, and thus obviate the need for aggressive interest rate hikes that typically accompany economic booms. This forward-thinking perspective allowed the U.S. to experience a prolonged period of robust expansion throughout the 1990s.

Warsh's Bold Parallel and a Stark Reality Check

The narrative gains a contemporary edge with the views of Kevin Warsh, a recent appointee to the Fed's leadership. Warsh is drawing a striking comparison between the transformative power of the internet in the 1990s and the current ascent of artificial intelligence. He suggests that AI could represent a similar technological leap, promising a surge in productivity that might naturally cool inflation and ease the pressure on monetary policy setters.

The ambition, it seems, is for the current Fed leadership to emulate Greenspan's masterful handling of the 1990s productivity boom. The idea is to adopt a tolerant stance on monetary policy, allowing the economy to benefit from the potential cost reductions and efficiency gains AI might unlock, rather than preemptively tightening conditions.

However, the path forward for Warsh is fraught with a significant hurdle: the stark difference in institutional standing between himself and Greenspan during their respective periods of influence. In the mid-1990s, Greenspan commanded immense authority. His reputation, built over years of navigating economic challenges and political pressures, made him an almost unassailable figure within the Federal Open Market Committee (FOMC). He could effectively steer policy discussions and persuade fellow policymakers to align with his vision.

Warsh, by contrast, is a relative newcomer to the Fed's top echelons. He lacks the decades of experience and the deep well of respect that Greenspan enjoyed. This disparity in standing means Warsh's perspective on embracing an AI-driven productivity surge might not carry the same weight within the FOMC. He faces the very real possibility of being outvoted by colleagues who may not share his optimistic outlook or his willingness to tolerate potential inflationary signals stemming from rapid technological advancement.

The consequence could be a central bank policy that Warsh himself disagrees with, a scenario almost unimaginable during the Greenspan era. This presents a critical test for the Fed's ability to adapt its policy framework to a potentially new economic reality, challenging the very notion of consensus-building at the heart of monetary decision-making.

Market Ripple Effects

The potential for a productivity surge driven by artificial intelligence, as suggested by Warsh's comparison to the 1990s internet boom, carries significant implications across financial markets. If AI can indeed deliver a substantial boost to output per worker, it could reshape investment strategies and currency valuations.

For traders and investors, this narrative presents a complex interplay of opportunities and risks. On one hand, a genuine productivity boom could fuel a sustained rally in equities, particularly in technology and growth-oriented sectors poised to benefit from AI adoption. Companies demonstrating clear advantages in AI implementation could see their valuations climb.

Conversely, the Federal Reserve's reaction to such a boom is a critical variable. If Warsh's view prevails and the Fed adopts a more accommodative stance, it could keep borrowing costs lower for longer, further supporting asset prices. However, if his influence wanes and the FOMC opts for more traditional inflation-fighting measures, higher interest rates could emerge sooner than anticipated, potentially dampening enthusiasm for risk assets.

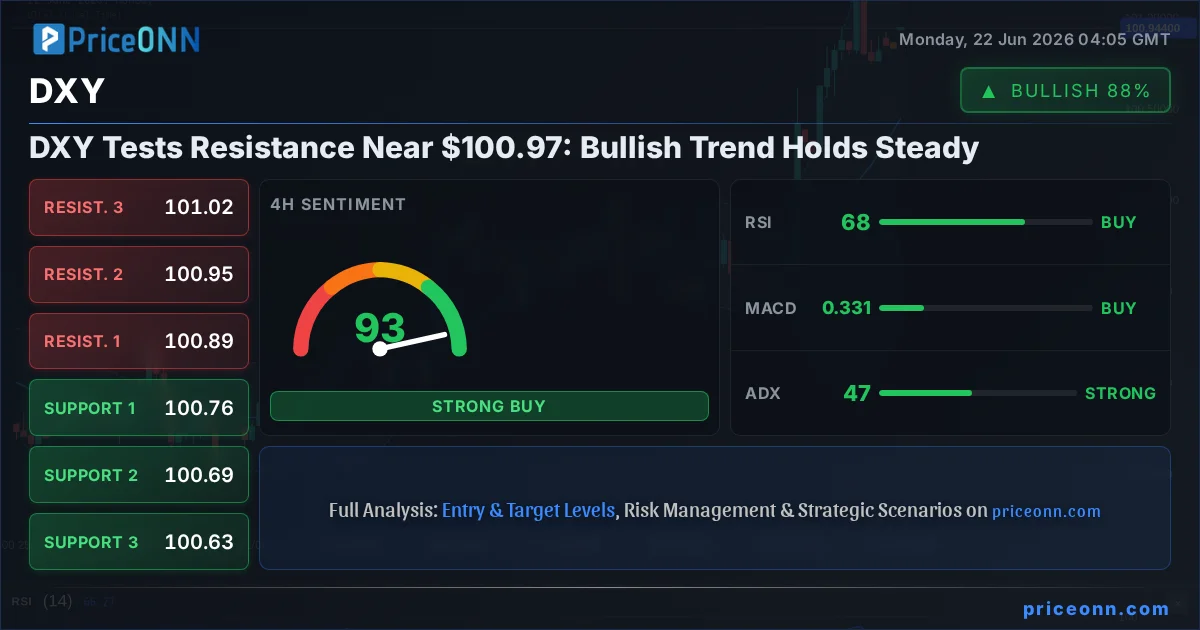

The U.S. Dollar Index (DXY) could also experience volatility. A strong productivity surge might initially boost the dollar on the back of economic optimism. Yet, if the Fed's policy response is perceived as too dovish compared to other central banks, it could exert downward pressure on the currency. Meanwhile, longer-term Treasury yields would be a key barometer; a sustained productivity expansion should theoretically cap yield increases, but any inflation fears could push them higher.

Finally, the commodity sector, particularly energy, might see demand influenced by the pace of AI-driven economic activity. While increased efficiency can sometimes curb energy consumption, the sheer scale of AI infrastructure development could offset this, creating complex demand dynamics. Monitoring the FOMC's internal debates and the public statements from its members will be crucial for discerning the likely path of monetary policy and its subsequent market impact.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelChicago Fed President Austan Goolsbee said the Federal Reserve’s primary challenge is determining whether inflation currently running well above target will gradually recede or remain stuck at elevated levels. Speaking on the Marketplace radio program, Goolsbee noted that policymakers are grappling with “an inflation problem that’s well above the target and has been going the […] The post Fed’s Goolsbee: Key Question Is Whether Inflation Stays at 3%-4% appeared first on ActionForex.

ECB Chief Economist Philip Lane emphasized on Tuesday that the central bank’s recent policy tightening should be viewed as a measured response to inflation risks rather than the start of an aggressive hiking cycle. Speaking before the European Parliament’s ECON committee, Lane acknowledged that progress toward resolving the conflict in the Middle East was encouraging […] The post Lane: ECB’s Response Is “Calibrated,” Not a “Huge, Gigantic” Tightening Push appeared first on ActionForex.

The EUR/USD pair traded near 1.1430 on Tuesday. The US dollar is refreshing its highs from March 2026, supported by expectations of further monetary policy tightening by the Federal Reserve, as well as cautious optimism surrounding negotiations between the US and Iran. An additional factor for the markets was Washington’s decision to grant Tehran a […] The post EUR/USD Remains Under Sellers’ Control as the Dollar Stays Strong appeared first on ActionForex.

Silver came under pressure following the Federal Reserve’s June meeting, at which policymakers kept interest rates unchanged at 3.50–3.75%. Nine of the 18 committee members still see the possibility of a rate increase this year, reinforcing expectations of further monetary tightening. The prospect of rising real yields reduces the appeal of non-interest-bearing assets such as […] The post Silver: Fed Tightens Its Tone as Price Returns to the Volume Profile Zone appeared first on ActionForex.

Inflows into US equity funds are heading towards a record high. Geopolitical and other fears continue to weigh on the S&P 500. Corporate earnings are rising, the economy is on a solid footing, and interest in AI shows no sign of waning. What else is needed to convince investors of a bright future for the […] The post S&P 500: the Higher It Climbs, the Greater the Fear appeared first on ActionForex.

Gold starts the week near 4,150 USD per troy ounce, its lowest level since 11 June. The precious metal has recorded a third consecutive weekly decline amid a stronger US dollar and growing expectations that the Federal Reserve may continue tightening monetary policy. The US currency refreshed its yearly high after the Federal Reserve’s June […] The post Gold Falls for the Third Consecutive Week: Is There Still Upside Potential? appeared first on ActionForex.

Following a period of heightened volatility in early June, investor attention in Ethereum has once again shifted towards institutional demand and the development of the spot ETF market in the United States. The funds launched last year continue to serve as one of the key channels for capital inflows into digital assets, while their daily […] The post Ethereum: Market Assesses the Strength of the Corrective Recovery appeared first on ActionForex.

Australia’s May inflation report delivered something for both doves and hawks. On the surface, the numbers looked encouraging. Headline CPI fell -0.7% mom and annual inflation slowed from 4.2% yoy to 4.0% yoy, both coming in below market expectations. Much of that improvement came from the collapse in fuel prices, with automotive fuel costs plunging […] The post Australia CPI Misses Expectations at 4%, Yet Core Inflation Sends Hawkish Signal appeared first on ActionForex.

US business activity accelerated in June, with the Flash Composite PMI Output Index rising from 51.5 to 52.2, its highest level in five months. The improvement was driven largely by manufacturing, where the Manufacturing PMI increased from 55.1 to 55.7, a 49-month high, while the Manufacturing Output Index climbed from 56.6 to 57.7, the strongest […] The post US PMI Improves as Middle East Tensions Ease and Energy Costs Fall appeared first on ActionForex.

Gold is once again approaching the level that has defined its battle with sellers for months. After falling back below 4,100, the precious metal is now drifting toward the 4,000 region, a major psychological level that has repeatedly halted deeper declines. This time, however, the pressure is coming from a source that Gold bulls may […] The post Gold’s $4,000 Floor Faces Fresh Threat as Tech Rout Fuels Dollar Surge appeared first on ActionForex.

The UK economy showed little sign of regaining momentum in June, with the Flash Composite PMI Output Index falling from 49.7 to 49.4, its lowest level in 14 months. The survey signaled a second consecutive month of contraction, driven primarily by weakness in the services sector. The Services PMI Business Activity Index declined from 49.3 […] The post UK PMI Signals Second Month of Contraction as Services Slump Deepens appeared first on ActionForex.

The Eurozone economy showed further signs of stabilization in June, with the Flash Composite PMI Output Index rising from 48.5 to 49.5, its highest level in three months. While the reading remained just below the 50 threshold that separates expansion from contraction, it pointed to a significant easing in the downturn. Services activity improved notably, […] The post Eurozone PMI: Economy Stays Out of Recession as Services Recover appeared first on ActionForex.