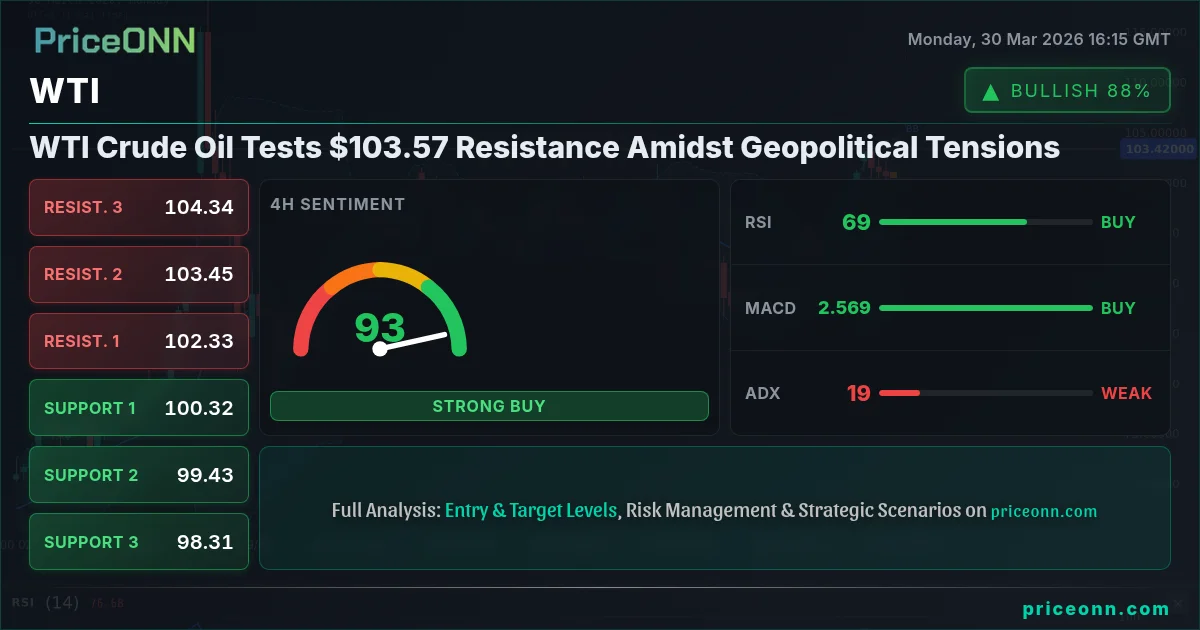

Will the Fed Pause as Oil Hits $110 and US Jobs Data Nears?

Global financial markets are navigating a pivotal week, often dubbed "Judgment Week," as the Federal Reserve's upcoming policy decisions hang in the balance. This crucial period is underscored by a confluence of significant economic indicators and external pressures, most notably crude oil prices breaching the $110 mark. Against this backdrop, the upcoming Non-Farm Payrolls (NFP) report, due this Friday, is poised to deliver a definitive verdict on the health of the U.S. labor market and, by extension, the Federal Reserve's interest rate trajectory for 2026.

Market Context: A Dual-Mandate Deadlock

Following a surprising contraction of -92,000 jobs in February, the markets are anxiously awaiting Friday's NFP print. The data will be instrumental in determining whether the labor market is experiencing a mere cooling trend or an outright freeze. This comes at a time when the Federal Reserve finds itself ensnared in a "Dual-Mandate Deadlock." The central bank is tasked with maintaining both price stability and maximum employment, objectives that appear increasingly at odds.

Any outcome from the NFP report that deviates from a "Goldilocks" scenario-a report indicating moderate job growth and stable unemployment-could force the FOMC into a challenging policy debate. This debate will likely pit the necessity of pausing interest rate hikes to support economic growth against the imperative to combat resurgent inflation, a scenario reminiscent of the Volcker era. The current economic environment presents a complex puzzle, where traditional monetary policy tools may struggle to address the multifaceted challenges.

Analysis & Drivers: The Evidence on Trial

This week's economic calendar is packed with high-stakes events that will provide critical evidence for the Fed's deliberations. The primary focus remains on the U.S. labor market and inflation indicators, alongside global economic signals.

1. The Verdict: US Nonfarm Payrolls & Unemployment (Friday, April 3)

After February's unexpected job losses, the Federal Reserve is desperately hoping for a stabilization in the upcoming NFP report. Analysts suggest a print between +50,000 and +80,000 jobs, especially if accompanied by upward revisions to January's figures, would allow the Fed to maintain its "Hawkish Hold" stance. Such a report would enable policymakers to characterize the 4.4% unemployment rate as a sign of normalization rather than a cause for alarm. However, a second consecutive contraction, for instance, a decline of -50,000 jobs, would signal a potential freefall in the labor market. This would put immense pressure on the Fed to consider rate cuts, irrespective of inflation concerns.

The critical "Stagflation Trap" within the NFP data lies in the Average Hourly Earnings. With an expected growth of 0.4% month-over-month, if job creation falters while wages continue to climb robustly, the Fed faces a difficult choice. Cutting rates in such an environment could exacerbate inflationary pressures, effectively surrendering the fight against rising prices. This scenario highlights the delicate balancing act the Fed must perform.

2. The Star Witness: ISM Manufacturing Index (Wednesday, April 1)

While the NFP report reflects the outcome, the Institute for Supply Management (ISM) Manufacturing Index offers insight into the underlying causes. The Prices Paid sub-index will be the most closely watched component. If this index remains elevated, particularly above the 70 level, while the New Orders index falls below the crucial 50 mark (indicating contraction), it would confirm a "Stagflation Filter." This suggests that cost-push inflation, potentially driven by global supply chain disruptions and geopolitical tensions like those in the Middle East, is seeping into the broader economy. Such a development would pose a significant challenge for the Fed, as traditional interest rate policy is ill-equipped to address supply-side inflation.

3. The Global Catalyst: Eurozone Flash CPI (Tuesday, March 31)

The preliminary Consumer Price Index (CPI) data for the Eurozone, scheduled for release on Tuesday, is another pivotal indicator. Analysts are closely monitoring this report as it could significantly influence the European Central Bank's (ECB) monetary policy and, by extension, the global economic outlook. Higher-than-expected inflation in the Eurozone might force the ECB to adopt a more hawkish stance, potentially leading to a stronger Euro and impacting trade flows. Conversely, signs of easing inflation could provide the ECB room for maneuver, perhaps even hinting at potential rate cuts later in the year, which could influence the Fed's own decision-making process through global market reactions.

The surge in oil prices to $110 adds another layer of complexity. Elevated energy costs can fuel broader inflation, putting further pressure on central banks to maintain restrictive monetary policies. This commodity price shock can also dampen consumer spending and business investment, acting as a drag on economic growth, thereby intensifying the Fed's "Dual-Mandate Deadlock."

Trader Implications: Navigating the Uncertainty

Traders are advised to brace for heightened volatility as these key data points are released. The immediate focus should be on the 4.4% unemployment rate and the Average Hourly Earnings growth figures within the NFP report. A print below +50,000 jobs combined with sticky wage growth would likely signal a "risk-off" sentiment across markets, potentially weakening the U.S. Dollar and boosting safe-haven assets.

Conversely, an NFP report that shows job growth between +50,000 and +80,000, coupled with moderating wage pressures, could support a "risk-on" environment, leading to a stronger dollar and potential gains in equity markets. The ISM Manufacturing Prices Paid index exceeding 70 would be a significant warning sign for inflation, regardless of the NFP outcome, potentially leading traders to reassess their long-term inflation expectations and currency positions.

Key support levels for the U.S. Dollar Index (DXY) to watch would be around the 104.00 mark, while resistance could emerge near 105.50. For major currency pairs, traders should monitor EUR/USD for potential moves towards 1.0800 if risk aversion increases, or a retreat towards 1.0700 on a stronger dollar. Similarly, GBP/USD could face pressure below 1.2500. The surge in oil prices to $110 adds a geopolitical risk premium that traders must factor into their commodity and currency strategies. Any indication of escalating tensions could further complicate the Fed's decision-making and currency valuations.

Outlook

This week represents a critical inflection point for both the Federal Reserve and the broader financial markets. The interplay between labor market data, inflation indicators, and the persistent rise in oil prices will heavily influence the Fed's immediate policy path. If the data points towards stagflationary pressures, the Fed may be compelled to maintain its restrictive stance longer than anticipated, even at the risk of slowing economic growth. Conversely, signs of a weakening labor market could force a pivot, potentially leading to a pause or even rate cuts, although the inflation backdrop makes this a complex proposition. Traders should remain vigilant, prepared to adjust their positions as new information unfolds, with the key levels and data releases this week serving as crucial guideposts.

Frequently Asked Questions

What is the significance of the $110 oil price for the Fed's decision?

Oil prices reaching $110 contribute to inflationary pressures, complicating the Fed's dual mandate. Higher energy costs can dampen economic activity while simultaneously pushing up the overall inflation rate, making it harder for the Fed to justify rate cuts aimed at supporting growth.

What is the 'Goldilocks' scenario for the upcoming Non-Farm Payrolls report?

A "Goldilocks" NFP report is one that indicates moderate job growth, ideally between +50,000 and +80,000, and a stable unemployment rate around 4.4%. This scenario would allow the Fed to maintain its current policy stance without exacerbating inflation or signaling a severe economic downturn.

How might the Eurozone CPI data affect the US Dollar?

Higher-than-expected Eurozone CPI could lead to a more hawkish stance from the ECB, potentially strengthening the Euro (EUR) against the US Dollar (USD). Conversely, softer inflation might prompt the ECB to consider easing, which could weaken the Euro and indirectly support the Dollar by influencing global market sentiment.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join Channel

PriceONN