Yen Jumps as Markets See Katayama’s Pension Fund Push as Structural Fix for Currency Weakness

Currency Market Jolted by Capital Flow Hint

A significant upward move in the Japanese Yen reverberated across global markets today. This surge followed remarks from Japan's Finance Minister, who indicated a desire to steer major pension funds, notably the colossal Government Pension Investment Fund (GPIF), toward increasing their exposure to domestic financial instruments. Although no concrete policy shifts were formally declared, the financial community interpreted these statements as a potential turning point in addressing one of the Yen's most entrenched structural vulnerabilities: the continuous outflow of capital seeking foreign assets.

The market’s swift reaction was not confined to currency trading desks. A robust rally swept through Japanese government bonds, affecting yields across the entire maturity spectrum. The 20-year yield, for instance, saw a notable decline of 11.5 basis points, settling at 3.75%. Similarly, the 10-year yield dipped 10 basis points to 2.775%. Even longer-dated maturities like the 30- and 40-year bonds experienced drops exceeding 8 basis points, underscoring the broad impact of this sentiment shift.

The Scale of GPIF and Its Global Shadow

This dramatic market response is intrinsically linked to the sheer magnitude of Japan's institutional investment power. The GPIF, recognized globally as the largest pension fund with assets under management approximating JPY 292.6 trillion, has, since its significant portfolio recalibration in 2014, maintained a relatively balanced allocation between domestic and international fixed income and equity holdings. That strategic pivot away from predominantly Japanese assets initiated a decade characterized by persistent capital outflows, as trillions of Yen were converted into foreign currencies to acquire overseas investments.

Consequently, Minister Katayama's recent commentary was perceived as potentially opening the door, however slightly, to a partial reversal of this long-standing trend. The implications for the Yen are multifaceted, suggesting a dual mechanism for bolstering the currency's standing.

Dual Channels Supporting the Yen

Firstly, a greater allocation towards Japanese domestic assets would necessitate the conversion of a portion of existing foreign currency reserves back into Yen. This action would inherently create sustained demand for the Japanese currency, independent of any direct intervention by monetary authorities. Such a move would offer a more organic form of support.

Secondly, an enhanced appetite for Japanese government bonds (JGBs) could provide crucial long-term stability to the domestic bond market. This is particularly relevant at a time when global investors are increasingly sensitive to rising yields at the long end of the curve and harbor concerns regarding Japan's fiscal trajectory. Therefore, fostering increased domestic investment could serve a dual purpose: strengthening the Yen while simultaneously alleviating pressure on the government's borrowing expenses.

Beyond Intervention A Structural Approach

This proposal aligns with Japan's broader search for alternative strategies beyond conventional foreign exchange intervention. Given the persistent interest rate differential, estimated at approximately 250-275 basis points between the U.S. Federal Reserve and the Bank of Japan, aggressive tightening by the BoJ appears improbable in the immediate future. By focusing on capital flows, policymakers gain another avenue to moderate the Yen's structural weakness without sole reliance on interest rate adjustments or direct market intervention.

However, the market's enthusiastic reaction today might prove to be premature if concrete policy follow-through fails to materialize. Minister Katayama's remarks focused on encouraging greater domestic investment rather than announcing specific portfolio overhaul directives. The GPIF operates autonomously, guided by a fiduciary duty to maximize long-term returns, and its strategic asset allocation is typically reviewed within its multi-year planning cycles, not in direct response to ministerial suggestions. History shows similar market reactions have faded quickly when policy actions did not materialize, as seen with recent speculation regarding Japan's intervention strategy.

Furthermore, even a substantial reallocation by the GPIF might not fully offset the significant interest rate differentials that continue to fuel global carry trades against the Yen.

Reading Between the Lines

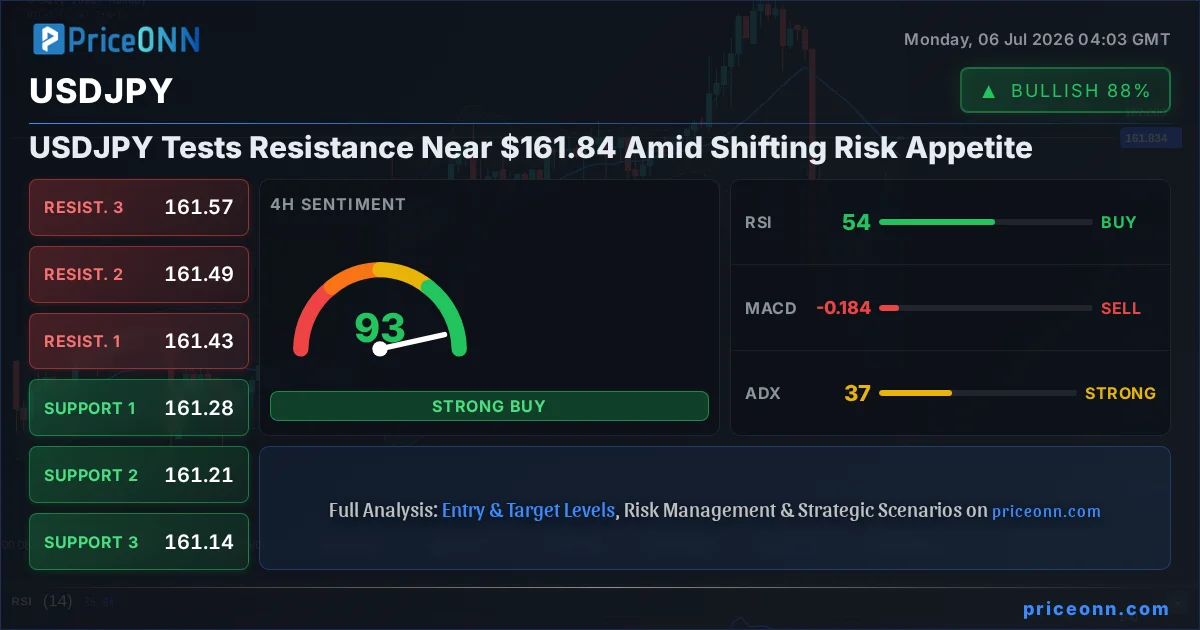

Technically, the sharp retracement in the USD/JPY pair offers a clearer picture of recent price action. The rebound from the 160.46 low appears to have concluded at 162.69, failing to surpass the prior high of 162.83. This decline from the recent peak is widely interpreted as the third wave within a larger consolidation pattern that is part of the overarching uptrend initiated from the 155.01 level.

While a deeper pullback towards 160.46 and potentially lower is not out of the question, significant support is anticipated to emerge around the 38.2% Fibonacci retracement level of the 155.01 to 162.83 range, situated at 159.84. This level is expected to contain any downside pressure. The long-term upward trend is projected to resume at a later stage, with the current movement seen as a temporary delay rather than a trend reversal.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelThe USD/JPY pair tumbles to around 161.50 during the early European trading hours on Friday. The Japanese Yen (JPY) edges higher against the US Dollar (USD) after the reports that Japan plans to encourage pension funds to increase their holdings of domestic financial assets.

The Japanese Yen (JPY) trades higher against the US Dollar (USD) despite renewed geopolitical risks.

The AUD/JPY cross trades in negative territory around 112.62 during the early European trading hours on Thursday.

Oil is back in the driver’s seat, and both the pound and the aussie are feeling its grip. The Bank of England held rates at 3.75% in June, but with UK inflation at 2.8% and crude oil climbing on renewed Middle East tensions, markets now lean towards a hike before year-end. Down under, the Reserve […] The post GBP/AUD Analysis: the Tug-Of-War Begins appeared first on ActionForex.

Rumours of talks between the US and Iran are dragging down the USD index. The ECB intends to act decisively on raising interest rates. The US dollar continued to retreat following Donald Trump’s statement that Iran is seeking a deal. Investors have encountered such rhetoric from the US president many times since April, and each […] The post The Dollar: Things Are Heading Towards De-Escalation appeared first on ActionForex.

The minutes from the Reserve Bank of Australia’s (RBA) June meeting, released on 30 June, suggested that policymakers are not yet ready to rule out further policy tightening. Board members noted persistent excess demand and broad-based inflationary pressures across the economy, leaving the door open for another interest rate increase if required. Against this backdrop, […] The post Australian Dollar Holds Above the Current Market Profile appeared first on ActionForex.

The NZD/USD pair trades in positive territory around 0.5775 during the early European session on Friday. The New Zealand Dollar (NZD) gathers strength to its strongest level in three weeks against the US Dollar (USD) on a hawkish rate hike from the Reserve Bank of New Zealand (RBNZ).

Silver price (XAG/USD) trades 0.4% higher to near $60.22 during the European trading session on Friday. The white metal gains as the US Dollar (USD) continues to remain under pressure amid hopes that the restart of the war between the United States (US) and Iran won’t long last.

The Swiss Franc (CHF) pares some of its early gains against the US Dollar (USD) during the early European trading session on Friday. The USD/CHF pair is 0.26% lower at around 0.8048 even after a slight recovery move.

The Indian Rupee (INR) extends Thursday’s recovery against the US Dollar (USD) in the opening session on Friday. The USD/INR pair falls further to near 95.22 as the US Dollar weakens as the restart of the war in the Middle East between the United States (US) and Iran won’t be prolonged.

The GBP/USD pair trades in positive territory around 1.3430 during the early European trading hours on Friday. The UK government leadership transition and growing expectations of further Bank of England (BoE) interest rate hikes underpin the British Pound (GBP) against the US Dollar (USD).

The EUR/USD pair attracts some buyers for the third consecutive day and touches a fresh weekly high, around the 1.1460 area, during the Asian session on Friday.