Analysts Warn China’s Oil Demand May Never Fully Recover

Demand Destruction Looms for Chinese Crude Market

A seismic shift appears to be underway in China's energy landscape, with projections suggesting a permanent dent in its massive crude oil appetite. Energy sector experts are flagging the accelerating transition to electric vehicles as a primary driver, predicting that demand may not simply pause but fundamentally shrink. This outlook challenges previous assumptions about the resilience of oil consumption in the world's second-largest economy and the largest importer of the commodity.

Consultancy Rystad Energy has put forth stark figures, estimating that China's oil consumption has already fallen by 200,000 to 600,000 barrels per day compared to pre-conflict levels. Their analysis suggests a significant portion of this reduction may be irreversible within the current year. Adding to this somber forecast, Energy Aspects anticipates a permanent loss of 300,000 barrels daily from China's usual oil intake.

The situation is further complicated by other contributing factors. FGE NexantECA forecasts a dramatic quarterly drop in Chinese oil imports, potentially reaching 3.3 million barrels per day. This steep decline is attributed to a confluence of issues: reduced activity at domestic refineries, the natural conclusion of seasonal inventory building, and a government policy restricting fuel exports. Beijing's ban on fuel exports, intended to bolster domestic supply, has inadvertently saturated the local market, thereby curating less need for imported crude as feedstock.

However, not all market watchers share the most pessimistic outlook. Kpler, for instance, suggests that Chinese refiners might soon increase their import volumes. This view is predicated on the idea that recent price surges, themselves a consequence of geopolitical tensions, compelled refiners to draw down existing stockpiles. To maintain strategic reserves and ensure a stable supply cushion against future shocks, these inventories would eventually require replenishment. This presents a potential counter-trend, though the underlying structural shift towards EVs remains a dominant narrative.

Reading Between the Lines

The divergence in forecasts from consultancies like Rystad Energy, Energy Aspects, FGE NexantECA, and Kpler highlights the inherent uncertainty surrounding China's future oil demand. While short-term factors such as refinery run rates and inventory levels can cause import fluctuations, the persistent growth of electric vehicle adoption presents a more profound, long-term challenge to oil demand. This trend could fundamentally alter global oil trade flows and pricing dynamics.

What this means for traders is a potential recalibration of long-term supply and demand expectations. A structurally lower demand from China, the world's largest oil importer, could exert downward pressure on global crude prices over time. This scenario directly impacts benchmarks like Brent Crude and WTI Crude, as well as the currencies of major oil-exporting nations such as the Canadian Dollar (CAD). Investors and traders should monitor China's EV sales figures and government policy statements on energy consumption closely. The key risk is mispricing the long-term impact of electrification, while the opportunity lies in anticipating the market's adjustment to a new demand paradigm.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelPresident Trump has ordered an investigation into possible price gouging at fuel stations, an investigation he announced in a social media post. “The big Oil Companies are not dropping their price at the pump commensurate with the sharply lower prices they are paying for Oil. Those prices are dropping like a rock! In other words, customers are being "gouged",” Trump wrote. “I have instructed the DOJ to immediately start looking into this. Gasoline prices better start going down a lot faster...

India is set to import a record-high volume of Russian crude in June as the Hormuz crisis and the U.S. waivers on Russia’s barrels have pushed the world’s third-largest crude importer to gorge on Moscow’s oil again. India has imported 2.6 million barrels per day (bpd) of Russian crude oil so far in June, according to preliminary vessel-tracking data from commodity analytics firm Kpler cited by Indian media. So far this month, Russian crude has accounted for as much as 53.5% of all Indian oil...

Indian Oil Corporation (IOC), the biggest refiner in the country, did not receive any bids in a tender to charter three tankers to pick up crude and gas from the Persian Gulf and ship the volumes through the Strait of Hormuz, trade sources with knowledge of the development told Reuters on Tuesday. Since the Strait of Hormuz tentatively reopened at the end of last week, vessel traffic has picked up, especially for outbound tankers that have been stuck for months in the Gulf. But many shipowners...

Iran is pitching its oil to Asian buyers outside China, contacting India, South Korea, and Japan, as the United States issued a temporary two-month waiver allowing Iranian oil sales, including in U.S. dollars, until August 21. As part of the 14-point memorandum of understanding with Iran, the United States on Sunday authorized the production, delivery, and sale of crude oil, petrochemical products, and refined oil products of Iranian origin through August 21, 2026. Representatives of the...

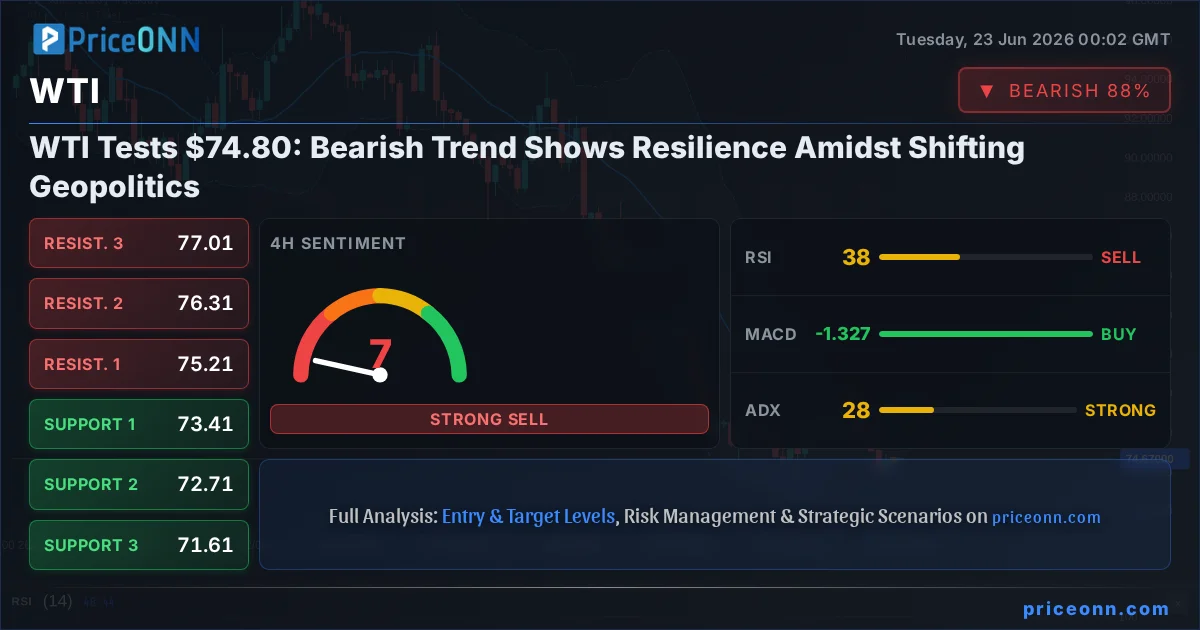

Crude oil prices extended their decline today, with Brent crude sliding to $77.51 per barrel at the time of writing, and West Texas Intermediate at $73.62 per barrel, on reports that the United States and Iran were making progress in their peace talks. The latest updates from the negotiations table include a report that the United States will waive sanctions on Iran’s oil industry for the 60-day duration of the cessation of hostilities agreed earlier this month. The two parties also agreed on a...

Threats from President Trump to bomb Iran again and Iranian negotiators leaving the talks in Switzerland once again clouded the outlook for one of the world’s busiest oil chokepoints. Talks are progressing, but the degree of uncertainty about global oil supply security remains high-because of the risk environment in the strait, of which most appear to be oblivious. Social media users have started calling Hormuz the Strait of Schrodinger, and with good reason. It is not only about whether the...

The outline of conditions and topics for a negotiated settlement of the U.S.-Iran conflict, called a Memorandum of Understanding (MOU) and signed by both sides last week, in all probability won't prevent the approaching energy cliff. That cliff will be the result of fast-depleting commercial and strategic inventories of oil and oil products around the world that have acted as buffers in the wake of the suspension of almost all tanker traffic through the Strait of Hormuz during the conflict -...

After Washington snatched Venezuela’s authoritarian president, Nicolas Maduro, in a daring January 2026 night raid, the country’s long road to recovery began. Under the leadership of Maduro’s former vice-president, Delcy Rodriguez, economically crucial oil production and exports are rising. President Trump is pressing Caracas to raise output, all while the U.S. president urges big oil to invest in the near-failed state. While doubts linger over whether production can return to historic highs,...

Europe’s benchmark natural gas prices rose by nearly 2% on Monday morning in Amsterdam as a heatwave in Europe is raising short-term power demand and the U.S.-Iran talks continue amid conflicting messages about the negotiations and renewed threats from U.S. President Donald Trump. The front-month Dutch TTF Natural Gas Futures, the benchmark for Europe’s gas trading, were up by 1.75% at $49.04 (42.83 euros) per megawatt-hour (MWh) early on Monday in Amsterdam trade, reversing some of the...

Iran isn’t wasting any time moving its oil out of the Gulf via the Strait of Hormuz after the U.S. lifted the naval blockade outside the chokepoint and the U.S. and Iran discuss a framework on a lasting peace deal. While Western shippers and insurers remain wary of the conflicting signals about how open the Strait of Hormuz really is, Iran is rushing to evacuate barrels it wasn’t able to push past the U.S. blockade over the past two months. At least three supertankers, carrying a total of 6...

Kuwait is offering naphtha for loading at its ports deep into the Persian Gulf in the first such tender in months, as Middle Eastern oil producers seek to raise shipments through the Strait of Hormuz. State-held Kuwait Petroleum Corporation (KPC) has issued a tender to sell naphtha cargoes to be picked up at Kuwaiti ports by buyers, Bloomberg reported on Monday, quoting a tender document it had seen. The Kuwaiti tender is a sign that the Gulf producers are hopeful that the Strait of Hormuz...

Malaysia’s state energy firm Petronas has made a natural gas discovery offshore Suriname, the country’s president said this week, as quoted by Reuters, expecting the Malaysian major to make the final investment decision on the development of Block 52 by the end of the year. “To date, we have made eight successful exploration discoveries, unlocking over more than one billion barrels of oil equivalent, while continuing advancing lower-carbon solutions, safe operations and investment in people,...