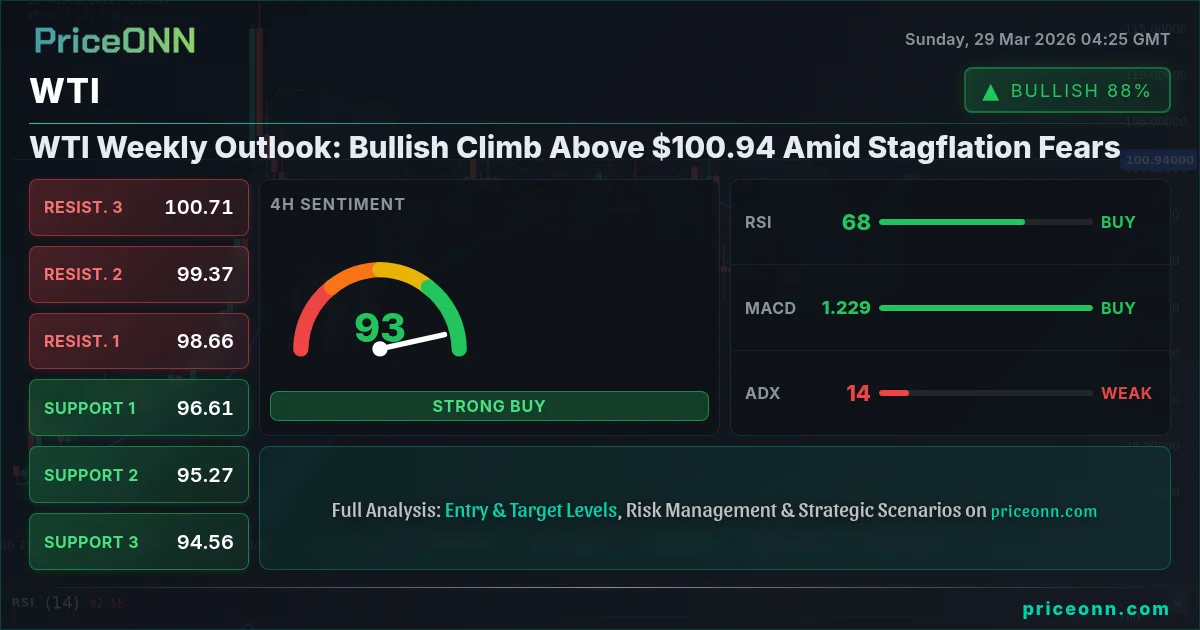

Is the Dollar Poised to Be the Global 'Wrecking Ball' Amid Stagflation Fears?

Global markets are increasingly signaling a return to a 1970s-style stagflationary environment, a scenario characterized by stubbornly high inflation coupled with sluggish economic growth. The most potent warning sign has been the emergence of a dual shock: a simultaneous rise in oil prices and Treasury yields. This is a departure from typical crisis responses where investors flock to bonds, driving yields down. Instead, current market data shows yields climbing alongside energy costs, indicating that inflation concerns are overshadowing traditional risk aversion.

Market Context

The underlying driver appears to be a protracted "war of attrition" in the Middle East, which is gradually infusing the global economy with persistent inflationary pressures. Unlike the sharp, short-lived price spikes of the past, the current dynamic involves elevated energy costs filtering through supply chains, impacting everything from transportation to food production. This presents a significant policy dilemma for central banks. Tightening monetary policy to combat inflation risks deepening an economic slowdown, while tolerating rising prices could lead to inflation becoming entrenched. However, unlike policymakers in the 1970s, today's central bankers are acutely aware of the lessons learned from past inflationary periods, suggesting a lower tolerance for sustained price increases.

Analysis & Drivers

The current confluence of rising crude oil prices and increasing Treasury yields suggests a structural shift in market dynamics. Analysts note that persistent energy price inflation, potentially driven by geopolitical supply disruptions, is a key factor. When oil prices approach the $120 per barrel mark, it acts as a significant drag on economic activity while simultaneously fueling inflation. This environment is particularly challenging for traditional safe-haven assets like gold. Market data indicates that in an environment of rising real yields, gold's appeal as a primary inflation hedge diminishes. Conversely, the U.S. Dollar may find support from higher interest rates and the nation's relative energy independence, positioning it as a potentially dominant currency. The "triple threat" of oil nearing $120, equities testing critical support levels, and Treasury yields approaching 5% would serve as strong confirmation that this stagflationary regime is firmly taking hold.

Trader Implications

Traders should closely monitor key price levels and economic indicators that could confirm or refute the stagflation narrative. For the U.S. Dollar, sustained strength would likely be seen as a "wrecking ball" to other currencies and risk assets, especially if the Federal Reserve maintains a hawkish stance due to inflation concerns. Key levels to watch include the Dollar Index (DXY) breaking above recent highs and sustained upward momentum in U.S. Treasury yields, particularly the 10-year yield approaching 5%. For currency traders, this suggests a potential environment favoring the USD against commodity currencies and those sensitive to global growth slowdowns. Investors should consider strategies that hedge against inflation and potential currency depreciation, while being wary of equity markets facing headwinds from higher rates and reduced consumer spending power.

Outlook

The coming weeks will be crucial in determining whether the current market conditions represent a temporary shock or a more durable shift towards stagflation. Upcoming economic data releases, particularly inflation figures and central bank commentary, will be closely scrutinized. If energy prices continue to climb and inflation proves persistent, central banks may be forced into a difficult balancing act, potentially leading to increased market volatility. The Dollar's trajectory will be a key barometer, with a strong performance potentially signaling a challenging period for global risk assets and other major currencies.

Frequently Asked Questions

What are the key indicators of the current stagflationary environment?

The primary indicators are a dual shock of rising oil prices, with benchmarks nearing $120 per barrel, and climbing Treasury yields, with the 10-year rate approaching 5%. This combination suggests inflation fears are dominating market sentiment.

How might the U.S. Dollar react to these market conditions?

The U.S. Dollar could emerge as a dominant force, acting as a "wrecking ball" for other currencies. Higher interest rates and relative energy independence provide support, especially if the Federal Reserve maintains a hawkish stance to combat persistent inflation.

What are the implications for gold in a stagflationary environment with rising yields?

In an environment of rising real yields, gold's traditional role as a primary inflation hedge may be diminished. Market data suggests that assets offering higher nominal returns, potentially supported by a strong dollar, could outperform gold if yields continue to climb past 5%.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join Channel

PriceONN