ECB Hikes As Expected, One More Likely in September

Market Pulse: Key Economic Data and Central Bank Actions

Traders are closely monitoring a slate of significant economic releases today, including the United Kingdom's April Gross Domestic Product figures. Preliminary Purchasing Managers' Index data suggests the UK economy maintained a growth trajectory through April before experiencing a slowdown in May. However, market consensus forecasts a slight contraction of -0.1% for April's GDP, a dip from the 0.3% expansion recorded in March.

Simultaneously, finalized inflation figures for the Eurozone in May are set to emerge from Germany, France, and Spain. These are expected to align with earlier preliminary estimates, which indicated a rise in headline inflation primarily driven by energy costs. Notably, Germany's energy component came in slightly below prior projections.

Adding to the Eurozone's focus, speeches from ECB officials Kocher, Rehn, and Nagel are scheduled. Market participants will be scrutinizing their remarks for deeper insights following the central bank's latest monetary policy decision. Across the Atlantic, US consumer sentiment will take center stage with the release of the preliminary University of Michigan Consumer Sentiment Index for June. The May index registered a weaker-than-expected final reading of 44.8, revised down from 48.2, falling short of the 49.5 consensus. A modest rebound to 46.0 is anticipated for June.

Yesterday's Market Moves and Geopolitical Undercurrents

The European Central Bank executed a widely expected 25 basis point rate hike, pushing the deposit facility rate to 2.25%. Following the decision, ECB President Lagarde emphasized the strength of the rate increase across various economic scenarios, minimizing concerns about growth while underscoring the upward risks to inflation. The central bank now anticipates a further rate hike to 2.50% in September, a shift from previous expectations of a July increase. Projections for two rate cuts in the first half of 2027 remain.

Meanwhile, geopolitical tensions surrounding Iran saw a significant de-escalation narrative emerge. President Trump announced that the US and Iran had finalized key points for a peace agreement, potentially to be signed soon, which he claimed would reopen the Strait of Hormuz for vital shipping lanes and halt planned US military actions. Iran, however, maintained that a definitive deal had not yet been reached.

This perceived easing of tensions prompted a market reaction, with Brent crude oil prices falling to approximately USD 89 per barrel and global equities experiencing a broad rally. In Norway, a softer-than-expected Regional Network Survey, showing a decline in capacity utilization and recruitment difficulties, coupled with previous CPI data, diminishes the likelihood of an immediate rate hike. The prevailing view is that Norway's policy rate peak has likely been reached.

Sweden's final May inflation data largely confirmed earlier estimates, with package holidays contributing an unusually early seasonal price increase. New measures of inflation excluding energy and accounting for constant taxes were also released, providing key inputs for the Riksbank's upcoming policy assessment.

In the United States, the May Producer Price Index (PPI) showed a month-on-month increase of 1.1%, heavily influenced by a 23.4% surge in gasoline prices. While core PPI appeared softer year-on-year at 4.9%, this was distorted by volatile trade services. Excluding this factor, core PPI indicated broader cost pressures building across goods and services, growing 5.1% year-on-year and 0.8% month-on-month. This report was viewed as more hawkish than the preceding CPI data, contributing to a slight uptick in US yields.

The Central Bank of Turkey maintained its overnight repo rate at 37% for the third consecutive meeting, meeting market expectations. Global equity markets posted strong gains, with cyclical stocks outperforming defensive sectors. The S&P 500 climbed 1.8%, the added 2.5%, and the Russell 2000 surged over 3%. This positive sentiment carried into Asian markets this morning, with South Korea's KOSPI showing a notable advance of over 8%.

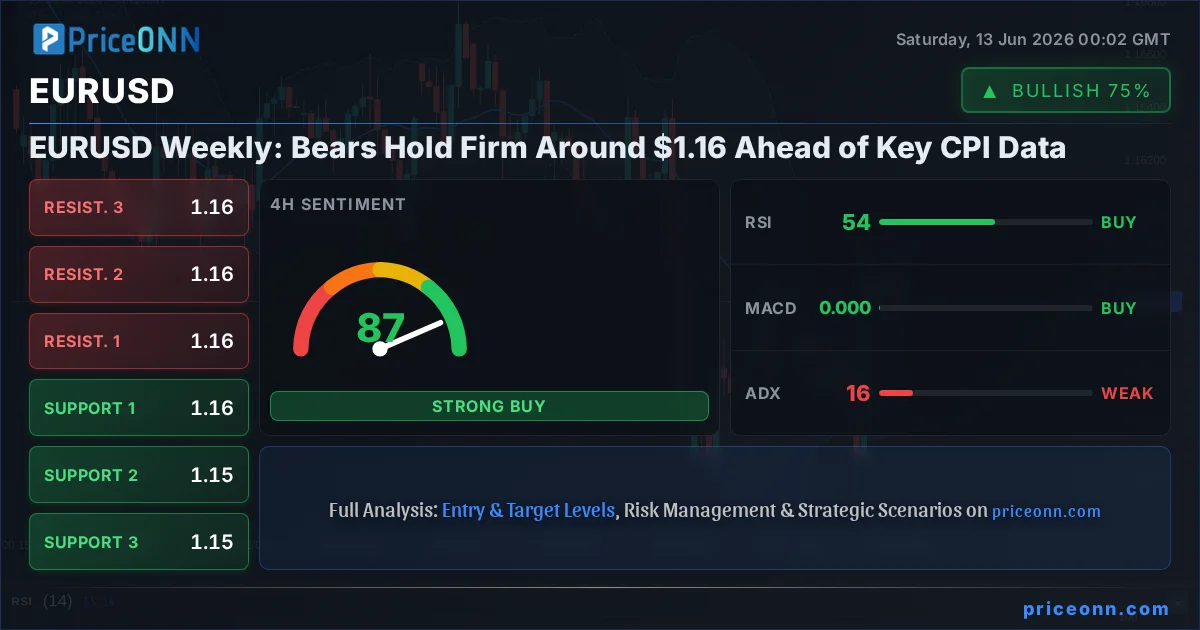

Financial markets experienced significant volatility. Initial risk aversion, triggered by threats of further US strikes on Iran, pushed EUR/USD lower towards 1.15. However, the sudden announcement of a potential US-Iran deal led to a sharp reversal, with EUR/USD climbing towards 1.16 as rates declined. The ECB's rate decision, while significant, was overshadowed by geopolitical developments. Given the unconfirmed nature of the Iran deal, market sentiment is expected to remain closely tied to geopolitical news.

Reading Between the Lines

The European Central Bank's decision to raise rates by 25 basis points was a foregone conclusion, but the accompanying statement signals a persistent hawkish stance. The emphasis on upside inflation risks suggests that further tightening is not merely possible but probable, with September now firmly in the crosshairs for another hike. This continuation of policy tightening, even with potential growth headwinds, underscores the ECB's primary mandate of price stability. The market's immediate reaction was muted, largely due to the overshadowing geopolitical narrative concerning Iran. However, underlying inflationary pressures, particularly evident in the US PPI data excluding volatile components, indicate that central banks globally are grappling with sticky price increases.

The potential de-escalation in the Middle East, if realized, could provide significant relief to energy markets, impacting inflation expectations and potentially influencing future central bank decisions. However, the uncertainty surrounding the confirmation of any deal means that energy prices, and by extension inflation, remain a key risk factor. For traders, monitoring the spread between headline and core inflation figures, especially in the US and Eurozone, will be critical. The divergence between the ECB's hawkish tone and the softer UK GDP forecast highlights varying economic conditions across major economies, creating opportunities in currency pairs like EUR/USD and GBP/USD.

The market's sensitivity to geopolitical events, as demonstrated by the sharp swings in oil prices and equity futures, suggests that risk sentiment will remain fragile. Investors should remain vigilant for shifts in geopolitical narratives, as these can rapidly alter market dynamics. The interplay between monetary policy tightening and geopolitical instability presents a complex trading environment. Key currencies to watch include the US Dollar Index (DXY), which may see renewed strength if safe-haven demand resurfaces, and commodity-linked currencies like the Canadian Dollar, which are sensitive to oil price fluctuations.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelAt its policy meeting on 11 June, the ECB raised its deposit rate by 25 basis points to 2.25%. This automatically raises the refinancing rate to 2.40% and the marginal lending rate to 2.65%. This decision was unanimous, based entirely on the forecasts of the Eurosystem’s economists and advocated by ECB Chief Economist Lane. The […] The post The ECB’s Interest Rate Hike Is More Than an Insurance Hike, but No Signal for a Start of a Tightening Cycle appeared first on ActionForex.

The European Central Bank meeting will clarify the outlook for EURUSD. The dollar is failing to capitalise on the favourable backdrop. The US dollar has ignored the escalation of geopolitical tensions in the Middle East and the fall in stock indices. Neither its status as a safe-haven asset nor the deterioration in global risk appetite […] The post The EURO: in the ECB’s Hands appeared first on ActionForex.

The European Central Bank also raised its inflation forecasts and cut its growth outlook.

USD/JPY rose to 160.52 on Thursday, marking its highest level since July 2024. The Japanese yen remains under significant pressure despite a notable acceleration in Japan’s producer price inflation. According to the latest data, Japan’s Producer Price Index (PPI) increased by 6.1% year-on-year in May, up from a revised 5.3% in April. The figure exceeded […] The post USD/JPY Continues Its Climb: Is There a Limit? appeared first on ActionForex.

On 11 June, the ECB is holding the second day of its Governing Council meeting. The interest rate decision will be announced at 14:15 CET, followed by a press conference by Christine Lagarde at 14:45 CET. Markets are focused on the possibility of a 25-basis-point rate increase to 2.25%. The case for further tightening is […] The post EUR/USD: ECB Meeting and Interest Rate Expectations appeared first on ActionForex.

As the chart shows, the US Dollar Index (DXY) has gained more than 4% from its January lows, with the move accelerating from February 2026 onwards. Today, the dollar finds itself at a technically and fundamentally critical point, one that could define the near-term direction not only of the greenback itself, but of equity indices, […] The post US Dollar Index Analysis: Dollar at a Crucial Point, What’s Next? appeared first on ActionForex.

Oil prices extended their sharp decline on today as markets grew increasingly confident that a breakthrough in US-Iran negotiations could eventually restore normal energy flows through the Strait of Hormuz. Brent crude slipped back into the $86-87 region, with the break below the psychologically important $90 level reinforcing the view that traders are beginning to […] The post Oil Collapses on Hormuz Optimism, EUR/CAD Rally May Be Just Getting Started appeared first on ActionForex.

Financial markets staged a powerful relief rally after US President Donald Trump abruptly called off planned military strikes against Iran and declared that diplomatic discussions had reached the “highest level of Iranian leadership.” Trump later suggested that a peace agreement could be finalized as soon as this weekend, potentially leading to the reopening of the […] The post Gold and Silver Hold Make-or-Break Zones After Trump’s Iran Pivot, but Bullish Reversal Remains a Work in Progress...

The ECB hiked policy rates by 25bp as expected, bringing the deposit rate to 2.25% at the June meeting. Lagarde highlighted the robustness of the decision to hike rates across a range of scenarios, downplayed growth risks, and emphasised upside risks to the inflation outlook. We now expect the ECB to deliver its second hike […] The post ECB Review: A Robust Hike, One More to Come appeared first on ActionForex.

We affirm our previously published view that the RBA will remain on hold in June, but increase rates in coming months given inflation risks. We affirm our existing expectation that the RBA Monetary Policy Board (MPB) will hold the cash rate steady at its June meeting next week. Although inflation remains above target, the previous […] The post RBA and Inflation View: June Hold Affirmed, Increases Still Ahead appeared first on ActionForex.

Key insights from the week that was. Our latest Westpac-MI Consumer Sentiment Survey proves the tense backdrop of elevated inflation, restrictive interest rates and heightened economic and political uncertainty is weighing heavily on the consumer mood. The headline index fell 2.9% to 80.6 in May, leaving sentiment stuck near pandemic-era lows. Cost-of-living pressures are the […] The post Cliff Notes: Stuck in the Moment appeared first on ActionForex.

The European Central Bank raised its key interest rates by 25bps as widely expected, and the accompanying statement delivered a clear message: the Middle East conflict is now a major inflation problem for the Eurozone. Explaining the decision, ECB said that “the war in the Middle East is generating inflation pressures” and that the rate […] The post ECB Hikes, Sees Higher Inflation, Lower Growth as Middle East Conflict Deepens appeared first on ActionForex.