Iraq's Energy Sector Faces Its Most Important Test in Decades

The Shifting Sands of Iraqi Energy Dominance

For years, the narrative surrounding Iraq's oil and gas sector has been confined to production volumes, OPEC adherence, and the sheer scale of its reserves. However, this perspective is rapidly becoming obsolete. The core drama unfolding now is not merely about barrels of oil but a profound struggle for national sovereignty, the assertion of state authority, and the very economic survival of the nation. The coming months are poised to be a defining period for the future of Iraq's vast hydrocarbon resources.

The government in Baghdad is embarking on an ambitious mission to consolidate and recentralize an energy industry long splintered by decades of conflict, pervasive corruption, the influence of paramilitary groups, entrenched regional rivalries, and systemic institutional frailty. Simultaneously, Iraq must navigate a precarious geopolitical landscape, balancing the demands of an assertive Iran, the growing autonomy sought by its Kurdish region, and the relentless pressures from global energy markets.

It presents a striking paradox: this Middle Eastern powerhouse possesses some of the planet's most significant oil and gas endowments. Yet, its energy trajectory will be shaped not by the earth's bounty but by the intricate web of political decisions. The Iraqi Ministry of Oil has ascended to a central role in Baghdad's broader state-building endeavors.

Since the beginning of 2026, federal authorities have intensified efforts to assert centralized command over exports, revenue streams, and critical infrastructure. A new leadership has taken the helm following recent elections. The elevated role of the State Oil Marketing Organization (SOMO) and other federal bodies signals a clear objective: to dismantle fragmentation and re-establish Baghdad's undisputed authority across the entire hydrocarbon value chain. The current Iraqi leadership understands that persistent political division directly translates into diminished revenues and a weakened strategic position.

Navigating the Hormuz Crisis and Export Vulnerabilities

The escalating tensions in the Strait of Hormuz have dramatically amplified the urgency for these internal reforms. Iraq finds itself among the nations most vulnerable to disruptions affecting Gulf energy transit. Prior to the regional flare-up, Baghdad managed exports of approximately 93 million barrels per month through this vital waterway. By April 2026, however, these shipments had plummeted to a mere 10 million barrels.

This stark reality has exposed the extraordinary fragility of Iraq's existing export infrastructure. Soaring insurance premiums, heightened security risks, and a shortage of available tankers converged to create an economic shockwave that Baghdad could no longer afford to ignore. For the first time in years, Iraqi policymakers are confronting a truth that energy analysts have long articulated: the nation cannot indefinitely rely almost exclusively on southern export terminals tied to a single, vulnerable geopolitical chokepoint.

This dawning realization is the primary catalyst behind the strategic imperative to revive exports via the Kirkuk-Ceyhan pipeline. The agreement forged in March 2026 between Baghdad and the Kurdistan Regional Government (KRG) transcended a simple export deal. The fundamental reality is that Iraq's energy security is inextricably linked to effective cooperation between Erbil and Baghdad, a fact now plainly acknowledged by the federal government.

Exports through Ceyhan have recommenced at a rate of roughly 200,000 to 250,000 barrels per day, with aspirations for significant increases in the near future. Joint technical committees are now operational, revenue is being channeled back into federal coffers, and both parties recognize the critical importance of maintaining the northern export routes. Nevertheless, premature optimism would be a grave miscalculation; this represents tactical alignment rather than strategic reconciliation.

The Kurdish Factor and Energy Diversification

The relationship between Baghdad and Erbil remains fundamentally precarious. The KRG continues to press for assurances regarding budget allocations, salary disbursements, trade regulations, and investor protections. Kurdish leadership consistently points to the necessity of addressing and eradicating security threats posed by militia groups operating near energy infrastructure as a prerequisite for restoring long-term confidence.

Baghdad, however, maintains its stance that all hydrocarbon revenues ultimately belong to the Iraqi state. Despite these underlying tensions, a degree of cautious optimism is warranted. The Hormuz crisis has engendered a rare convergence of interests: Baghdad requires functional northern export routes, while the KRG needs a steady revenue stream. International oil companies demand predictability, Turkey seeks the restoration of transit volumes, and Washington advocates for enhanced federal-KRG collaboration. It appears that for the first time in many years, all key stakeholders stand to benefit from a stable and operational export framework.

This dynamic extends to natural gas development. For decades, Iraq has presented a curious paradox, being a major energy producer yet heavily reliant on gas and electricity imports. Significant volumes of associated gas are flared daily, even as domestic demand continues its upward trajectory. In light of the evolving regional geopolitical and security environment, Baghdad now views gas development as both an economic necessity and a strategic imperative. Every cubic meter of domestically produced gas promises to lessen Iraq's dependence on Iranian imports and bolster national energy security.

This is precisely where the Kurdish region could emerge as a pivotal component of Iraq's future energy landscape. The KRG holds substantial untapped gas reserves that could satisfy domestic Iraqi needs, fuel industrial growth, and potentially support future exports to Turkey and Europe. European and other Western governments are increasingly seeing Kurdish gas development as a pathway to reducing Iraq's reliance on Iran, while simultaneously aiding Europe's own efforts to diversify away from Russian and other external gas suppliers. Consequently, the strategic importance of Kurdish gas has surged considerably over the past two years.

Geopolitical Headwinds and Investor Confidence

However, these promising developments cannot entirely eclipse the persistent Iranian influence. Iran remains the single most significant external factor shaping Iraq's political and energy landscape. The deep entanglement between Iran and Iraq is evident through extensive trade, electricity imports, religious networks, political alliances, and security structures. Recent sanctions imposed on Iraqi officials and allegations concerning Iranian-linked oil networks have once again underscored the difficulty of disentangling Iraqi energy policy from the broader regional geopolitical currents.

Baghdad's central challenge lies not solely in Iranian influence but in the pervasive presence of Iran-aligned militias operating within its borders. The new Iraqi leadership has pledged to reinforce state authority and bring all armed factions under government control. While some militia elements have indicated a willingness to engage with reform initiatives, others remain deeply entrenched within political, security, and economic establishments. Any emerging optimism regarding factions exploring a separation from overt militia affiliations must be tempered by the reality that institutional power built over two decades cannot be dismantled overnight.

For international investors, both Western and otherwise, this volatile situation represents the paramount concern. Major oil companies can effectively manage geological risks and price volatility. They can even navigate regulatory uncertainties. The critical obstacle they find insurmountable is the risk of missile attacks, interference from militias, political intimidation, and infrastructure sabotage. The ensuing weeks and months will serve as a crucial test for Iraq.

If Baghdad can successfully strengthen state authority without provoking direct confrontation with militia elements, investor confidence may see an uplift. Conversely, should tensions between Washington and Tehran escalate, mirroring current trends, Iraq is predictably expected to become a favored theater for proxy competition once more. In such a scenario, pipelines, oil fields, export terminals, and foreign-operated facilities would inevitably become targets.

The wider regional environment adds another layer of complexity. The closure of the Strait of Hormuz has fundamentally altered Iraq's strategic calculations. Even as regional tensions subside, policymakers now grasp that the previous operational model is unsustainable. Baghdad must actively pursue alternative export routes, pipeline expansions, and new accords with Turkey. Discussions involving international energy firms, including prominent American corporations, highlight Iraq's ambition to boost production capacity towards 5 million barrels per day while simultaneously advancing gas development. Yet, strategic blueprints and optimistic projections will inevitably collide with a formidable list of practical obstacles.

The existing Iraq-Turkey pipeline framework faces inherent uncertainties as long-standing agreements approach their expiration dates. Furthermore, the infrastructure investment required will be immense, amounting to several billion dollars. Security concerns are also projected to persist for an extended period. Despite these challenges, the overall direction of travel is increasingly apparent: Iraq is actively seeking diversification, redundancy, and enhanced strategic autonomy.

Reasons for Cautious Optimism

The narrative surrounding Iraq's energy sector has for years been dominated by a relentless series of crises: the rise and fall of ISIS, protracted budget disputes, dramatic oil price collapses, pervasive Iranian influence, militia violence, pipeline shutdowns, and political inertia. However, at present, perhaps for the first time in a decade, there are emerging signs that structural incentives are aligning in favor of reform. Baghdad acknowledges the critical need for strengthened institutions, including a functional security apparatus. Concurrently, the KRG recognizes the imperative of cooperation. International investors perceive the immense scale of the opportunity. Turkey values the potential for Iraqi exports. Even regional players are increasingly comprehending that a stable Iraqi energy sector benefits all parties involved.

The potential rewards are substantial. Within the vast energy landscape of the Middle East, Iraq remains one of the few nations capable of materially increasing global oil production over the next decade. Its natural gas reserves are largely untapped, and its petrochemical sector offers significant avenues for future growth. Geography further enhances its strategic position, acting as a crucial nexus connecting the Gulf, Turkey, Europe, and the Eastern Mediterranean.

For the Kurdish region, the outlook is equally promising, provided that political agreements can be sustained. The synergy of oil exports, gas development, proximity to Turkey, and growing international interest in energy diversification could transform the KRG from a persistent political challenge into one of Iraq's most valuable economic assets. While optimism is justifiable, the practical realities remain formidable. Iranian influence, even if the current regime in Tehran faces internal pressures, will endure. Iraqi Shia militias will not vanish overnight, and the disputes between Baghdad and Erbil are far from resolved. Regional instability is likely to resurface periodically, irrespective of developments like a US-Iran accord or a change in Tehran's leadership.

Nevertheless, the most significant development is that Iraq's leadership is finally beginning to address the deep-seated structural weaknesses that have hampered the sector for decades. The next crisis originating in Tehran, Washington, or Erbil will not unilaterally determine the future of Iraq’s oil and gas industry. Instead, if managed effectively, its future will be dictated by Iraq's capacity to forge institutions more resilient than the political forces that have historically sought to divide it.

Market Ripple Effects

This pivotal moment for Iraq's energy sector carries significant implications beyond its borders. The push for greater energy independence and export diversification directly impacts regional power dynamics and global energy flows. Traders and investors should closely monitor how Baghdad navigates the complex interplay between federal control, Kurdish autonomy, and external geopolitical pressures.

The renewed focus on the Kirkuk-Ceyhan pipeline is a key indicator. Its successful operation and expansion could alleviate some pressure on global oil prices, particularly for European benchmarks like Brent Crude, by offering an alternative supply route less susceptible to Strait of Hormuz disruptions. Additionally, developments in Iraq's natural gas sector, especially if Kurdish gas flows increase, could influence European gas prices and further reduce dependence on Russian supplies, potentially impacting the Dutch TTF futures contract.

The ongoing struggle to assert Baghdad's authority over all hydrocarbon revenues and infrastructure is critical. Should Baghdad succeed in centralizing control and mitigating militia interference, it could unlock significant investment potential for international oil companies and boost Iraq's overall production capacity. This, in turn, could exert downward pressure on global oil prices, particularly if it leads to a substantial increase in output towards the targeted 5 million bpd. Conversely, any escalation of internal conflict or renewed proxy tensions involving Iran could lead to supply disruptions, causing price spikes in crude oil and heightened volatility across energy markets. The Iraqi Dinar (IQD) exchange rate will also be sensitive to the success of these energy reforms and the resulting fiscal stability.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join ChannelThe Strait of Hormuz has become the pressure point of the global energy system. The war has already deprived global markets of 1 billion barrels of crude oil and petroleum products. Supply from the Middle East has been severely disrupted, and there is now rising uncertainty around Chinese refining projects and global inventories. For governments, part of the answer to this strategic crisis may now begin much closer to home. While energy security is often discussed from the top down – and...

Kuwait appears to have joined a growing bunch of Middle Eastern oil and gas producers that have moved to ship energy cargoes in dark mode through the Strait of Hormuz. The liquefied petroleum gas (LPG) carrier Gas Umm Al Rowaisat, which is owned by the national Kuwait Petroleum Corporation, has passed through the Strait in recent days, then transferred the cargo onto another ship which is currently en route to an Indian port, vessel-tracking data

U.S. Energy Secretary Chris Wright just gave the market a number that helps explain why Brent crude isn't trading at $150 per barrel. Speaking at a Bloomberg Energy event in Houston on Friday, Wright said the U.S. military is now helping move roughly 7 million barrels per day (bpd) of oil out of the Persian Gulf. According to Wright, that's about half of the oil that remains stranded following the disruption of tanker traffic through the Strait of Hormuz during the ongoing U.S.-Israeli conflict...

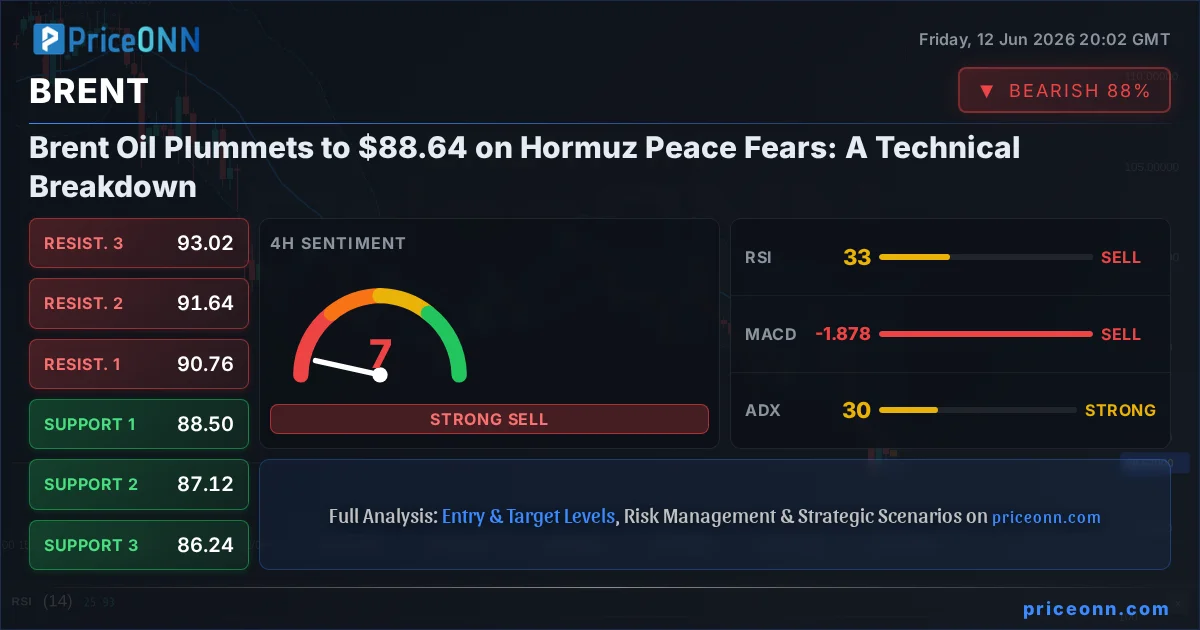

Oil prices slid to a two-month low as conflicting signals from Washington and Tehran fueled uncertainty over a potential U.S.-Iran deal, keeping traders on edge throughout a volatile week. Friday, June 12, 2026 In a particularly volatile trading week, the allocation of roles between Iran and the United States seemed to have switched constantly. If an impending deal was announced by US President Trump, Tehran would deny it, and reversely if the Iranian leadership broke the media silence with...

European buyers aren’t committing to long-term LNG supply agreements with U.S. exporters despite the ongoing EU phase-out of Russian gas imports and the supply crisis in the Middle East. U.S. developers and proponents of new LNG export facilities in America have been trying to lock in long-term supply deals with European importers, with little success so far this year, U.S. executives have told Bloomberg. The Europeans are interested in discussions, but not really committing to long-term supply...

Norway has intensified its charm offensive to persuade the European Union to drop its ban on Arctic drilling by campaigning that oil and gas resources in the High North would be better for the energy security of its closest ally than LNG supplies from the Middle East or the United States. Norway, which is not a member of the EU but is the biggest gas supplier to European markets, has been lobbying the bloc this year to drop its opposition to drilling in the Arctic. The Iran war and the biggest...

The on-and-off U.S. sanctions on Russian oil and the flipping U.S. position regarding India’s oil purchases from Russia highlight the double standards of the Western nations, Indian Foreign Minister S Jaishankar said on Friday. India turned en masse to Russian oil in 2022, when the U.S. and the EU imposed sanctions on Moscow due to the invasion of Ukraine. Four years later, India is a major buyer of Russia’s crude and Russia is India’s single-largest oil supplier. “At that time, the US...

India may be on track to miss its target for budget deficit for the first time since 2021 as the oil supply shock pressures government coffers. The government of the world’s third-largest crude oil importer is preparing to exceed its own deficit target from early this year as the Middle East crisis is testing the resilience of public finances amid soaring energy import bills, an Indian official with knowledge of the plans told Bloomberg on Friday. India may allow the budget deficit to widen to...

Oil prices plunged by more than 4% early on Friday as the market hopes the U.S. and Iran have made progress toward a peace deal. As of morning trade in Europe, the international benchmark, Brent Crude, had slipped by 4.34% at $86.36, extending the losses from Thursday when U.S. President Donald Trump called off a strike on Iran, claiming that a deal had been reached. The U.S. benchmark, WTI Crude, had dipped by 4.47% at $83.88. Both benchmarks were headed to a three-month low amid one of the...

(RTTNews) - Reversing yesterday's surge, crude oil prices have plunged on Thursday after U.S. President Donald Trump recalled his earlier orders to attack Iran hard.

OPEC is sticking to its view that the oil market will remain relatively tight through next year, with demand growth expected to continue outpacing non-OPEC+ supply additions despite months of war-related disruption and elevated prices. According to OPEC's June Monthly Oil Market Report released on Thursday, crude production from countries participating in the Declaration of Cooperation averaged 33.13 million barrels per day in May, down 190,000 bpd from April based on secondary-source...

Hengli Petrochemical, the privately-owned Chinese refiner that was sanctioned by the U.S. in April over allegedly buying Iranian oil, is looking to buy crude from other Middle Eastern producers and West Africa, Reuters reported on Thursday, citing trade sources. Hengli Petrochemical, one of China's largest independent refiners which operates a refinery in Dalian with the capacity to process 400,000 barrels per day of crude, was sanctioned by the U.S. Department of the Treasury's Office of...