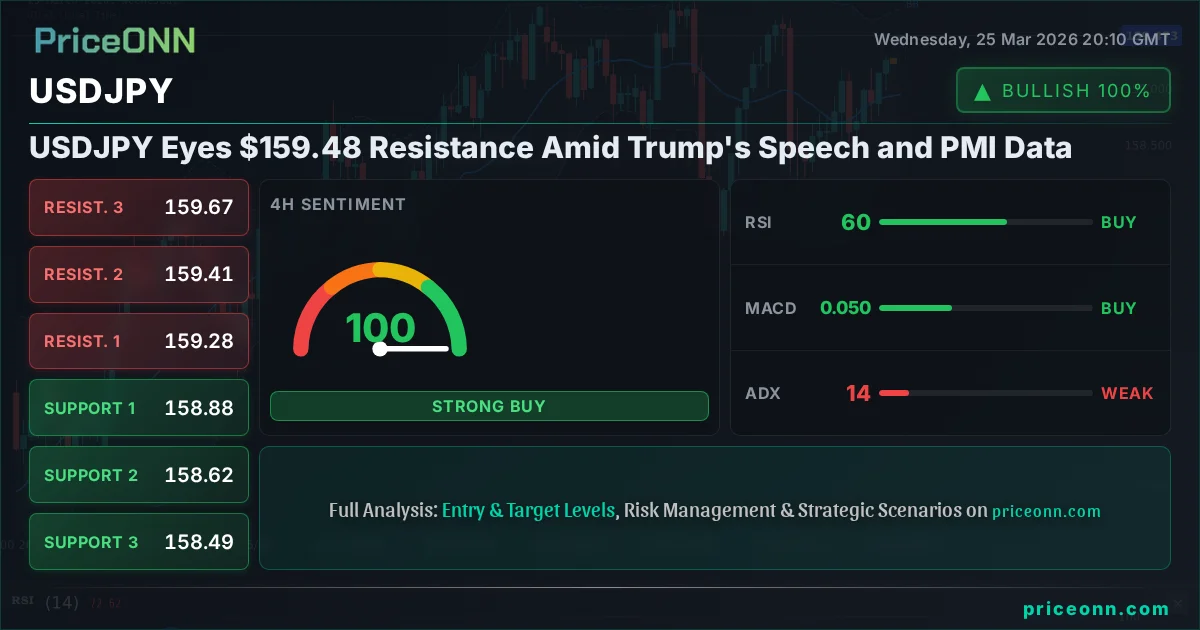

Japanese Yen hangs near YTD low vs. USD amid Middle East tensions, intervention fears

Yen Caught in Crosswinds of Global Instability

The Japanese Yen, a currency traditionally sought for its safe-haven appeal, finds itself precariously positioned near its lowest point against the US Dollar this year. This Thursday, during the Asian trading session, the USD/JPY pair was observed consolidating in the mid-159.00s, a region uncomfortably close to the yearly peak it tested earlier in the month. This delicate balance reflects a confluence of powerful forces, from escalating geopolitical risks to the ever-present possibility of direct market intervention by Japanese authorities.

Several key drivers typically dictate the Yen's trajectory. Foremost among these are the monetary policy stances of the Bank of Japan (BoJ) relative to its global counterparts, particularly the US Federal Reserve. Interest rate differentials, a widening or narrowing of yield gaps between Japanese and US sovereign debt, play a critical role. Furthermore, broader market sentiment, specifically risk-on versus risk-off appetite among global investors, significantly influences capital flows into or out of the Yen. The BoJ itself holds a mandate that includes maintaining currency stability, and its direct actions in the foreign exchange market, though infrequent, can send powerful signals. Historically, such interventions have often aimed at curbing excessive Yen depreciation, though they are approached with caution due to potential diplomatic repercussions with major trading partners.

Policy Divergence and the Yen's Long Slide

For much of the past decade, the BoJ's commitment to an ultra-accommodative monetary policy stood in stark contrast to the tightening cycles pursued by many other major central banks. This divergence fueled a significant widening of the yield gap between 10-year US Treasuries and their Japanese government bond equivalents. The result was a persistent tailwind for the US Dollar, pushing the USD/JPY pair steadily higher and causing the Yen to languish against its major peers. The economic rationale was straightforward: higher yields in the US attracted capital away from Japan, weakening the Yen.

However, recent shifts in policy have begun to alter this dynamic. The BoJ's gradual move away from its ultra-loose framework, initiated in 2024, coupled with anticipated or actual interest rate cuts by other key central banks, is starting to narrow these yield differentials. This recalibration offers some foundational support for the Yen, suggesting that the era of extreme policy divergence may be drawing to a close. Yet, this potential support is currently being overshadowed by other, more immediate market pressures.

The Bigger Picture

The current weakness in the Yen, despite nascent signs of policy normalization, highlights the potent influence of global risk aversion. Typically, during periods of heightened geopolitical uncertainty, like the ongoing tensions in the Middle East, investors flock to perceived safe-haven assets. The Japanese Yen has long been considered one such haven, owing to Japan's stable political environment and its status as a major creditor nation. When global markets become turbulent, capital is expected to flow into the Yen, strengthening its value.

The fact that the Yen is weakening, not strengthening, under these conditions speaks volumes about the dominant market forces at play. The lure of higher US yields, even if narrowing, combined with the immediate impact of geopolitical fears on risk sentiment, appears to be outweighing the Yen's traditional safe-haven status. This unusual dynamic forces traders to reconsider established correlations and look for new indicators of market direction. The market is grappling with whether the safe-haven narrative for the Yen still holds true in the face of aggressive monetary policy divergence and significant global instability.

Market Ripple Effects

This persistent pressure on the Japanese Yen has considerable implications beyond the USD/JPY cross. For instance, a weaker Yen can make Japanese exports cheaper, potentially boosting the earnings of major Japanese corporations across sectors like automotive and electronics. This could provide a tailwind for the Nikkei 225 index, although the overall impact depends on global demand and the specific earnings outlook for these companies.

Conversely, the weakening Yen also increases the cost of imports for Japan, including vital energy resources like crude oil. This could exert upward pressure on Japanese inflation metrics. On the global stage, the sustained strength of the US Dollar, partly fueled by the Yen's weakness, can impact other currency pairs. Emerging market currencies, often sensitive to dollar strength and global risk appetite, may face renewed headwinds. Furthermore, the US Treasury market, already sensitive to yield differentials and Fed policy expectations, will continue to be a key barometer for the direction of the USD/JPY pair.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

Join Channel