OPEC Oil Production Falls to Lowest Level Since 2000

The number is jarring even by historical standards. OPEC crude oil production has collapsed to just 16.13 million barrels per day in May, a reading that ranks as the lowest since 2000. What makes this figure particularly striking is its context: it falls below even the production floor touched during the Covid lockdowns of 2020, when demand evaporated almost overnight. This time, the shortage is not about collapsed demand. It is about war.

One structural note accompanies the data: the May figure excludes the UAE, which formally exited OPEC on May 1. That departure removes a meaningful volume from the headline count, but the underlying damage across the remaining membership is real and independently severe.

A 70% Freefall in Iraq's Heartland

The single most dramatic data point in the May survey belongs to Iraq. OPEC's second-largest producer by output has watched its southern fields lose 70% of their capacity since the outbreak of the U.S. and Israeli military campaign against Iran. Where Iraq was averaging 4.3 million barrels per day before the war started, it is now producing just 1.3 million bpd. That is a daily shortfall of three million barrels from one country alone.

Iran sits at the origin point of the disruption. Exports from Tehran have fallen to their lowest level in six years, driven by a U.S. naval blockade deployed in response to Iran's closure of the Strait of Hormuz. The passage closure did not confine its damage to Iran alone. Other Gulf states whose export infrastructure depends on free movement through the strait felt the impact as well, deepening OPEC's collective production shortfall across the region.

Venezuela and Nigeria Step Into the Void

Not every OPEC member is suffering. The cartel's Western Hemisphere producers, geographically removed from the Middle Eastern conflict, are quietly expanding output.

Venezuela exported an estimated 1.25 million barrels per day in May, a 0.7% rise from April's 1.23 million bpd. The longer view is even more telling: that figure represents a 61% surge against the same month in 2025. For a country that spent years mired in sanctions-induced decline, the rebound is substantial.

Nigeria reported oil and condensate production of 1.66 million barrels per day in May. Crude alone reached 1.49 million bpd, placing the West African producer just within range of its OPEC+ quota. Both countries represent rare bright spots in a picture otherwise dominated by loss.

Quotas on Paper, Shortfalls in Reality

OPEC+ voted earlier this month to raise its collective production quota by 188,000 barrels per day for July. Since April, the group has added 600,000 barrels per day to its approved ceiling. The intention is clear enough. The execution is the problem.

Actual production across the cartel remains constrained by physical reality: pipelines disrupted, export terminals operating at reduced capacity, and the war showing no immediate signs of resolution. Quota decisions reflect what the group wants to produce. The May data reflects what it actually can.

Market Ripple Effects

A supply disruption of this magnitude touches far more than the crude oil benchmark. Traders and investors tracking related markets should watch several interconnected dynamics as this situation develops.

Brent crude and WTI carry a war risk premium that will shift with any news related to the conflict's direction. A diplomatic breakthrough and Strait reopening would likely trigger a sharp price reversal; further escalation involving additional Gulf producers would push the supply gap wider and prices higher.

- USD/CAD: The Canadian dollar has a well-documented positive correlation with oil prices. A sustained supply crunch at this level could provide structural support for CAD against the U.S. dollar.

- Energy equities: Producers outside the conflict zone, including U.S. shale operators and North Sea drillers, stand to benefit from the elevated price environment while Gulf-region competitors remain constrained.

- Inflation expectations: Crude prices feed directly into headline CPI data. A prolonged price elevation complicates the rate-cutting path for the Federal Reserve, the ECB, and other major central banks.

- Gold: Geopolitical tension of this magnitude historically lifts safe-haven demand. Until a credible de-escalation signal emerges, gold retains a supportive backdrop from this conflict.

The critical variable to monitor is diplomatic, not economic. Ceasefire signals would reprice the oil risk premium quickly. Absent those signals, the gap between OPEC's paper quota and its physical barrel count will remain one of the defining features of the oil market through the second half of 2026.

Track markets in real-time

Empower your investment decisions with AI-powered analysis, technical indicators and real-time price data.

Join Our Telegram Channel

Get breaking market news, AI analysis and trading signals delivered instantly to your Telegram.

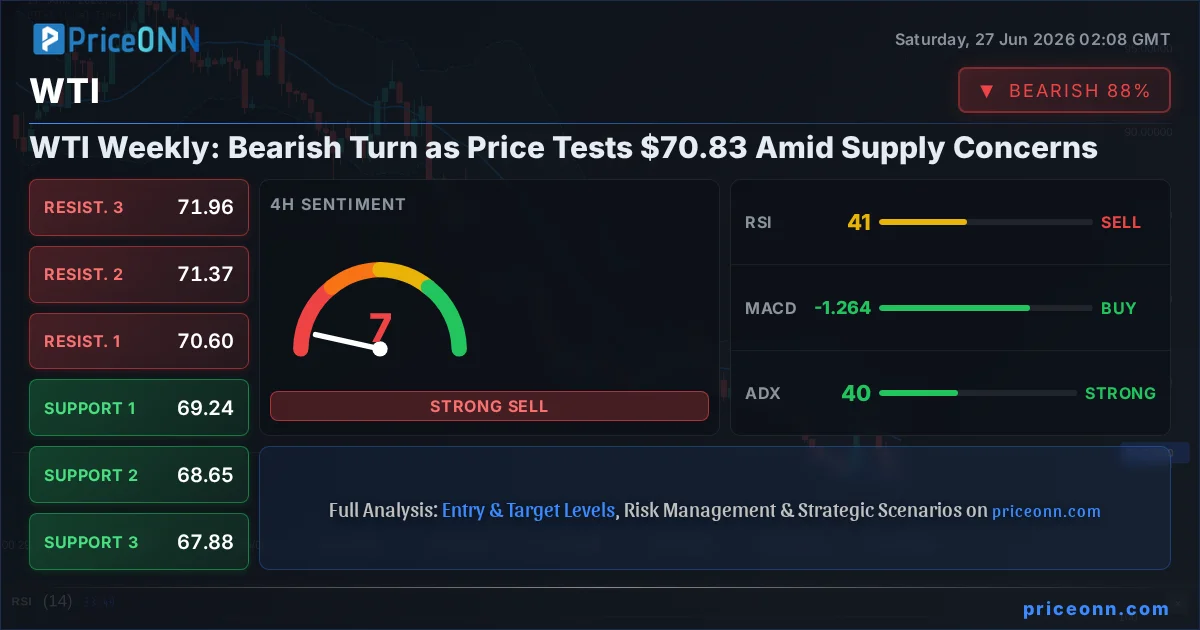

Join ChannelAugust WTI crude oil futures kept falling sharply during the week ending June 26. Traders continued to take out the extra price they had added earlier because they worried about possible supply problems in the Middle East. The contract moved between a high of $78.14 and a low of $68.90 before finishing at $71.53. That was down $3.99, or 5.28 percent, from the week before. The selling went on for most of the week. Traders stopped focusing as much on the chance of oil supplies getting cut off in...

According to a senior oil ministry official, Iraq will be compelled to consider all available options if its OPEC quota is not significantly increased, Reuters reports.

Oil prices tumbled as markets bet Strait of Hormuz disruptions will ease, with Brent down 10% on the week and Middle East crude benchmarks slipping into contango. Friday, June 26, 2026 Whilst ship transits through the Strait of Hormuz remain a fraction of their previous norm (130-140 transits per day), plunging crude oil prices suggest the commodity markets anticipate that flows would start to recover sooner than later. The two Middle Eastern crude benchmarks, Dubai and Murban, have flipped...

European officials are expected to visit Baghdad in the coming weeks for high-level talks on energy cooperation, just hours after Iraq warned it could leave OPEC unless the producer group grants the country a higher production quota. According to Iraqi sources cited by Shafaq News, the discussions will focus on expanding cooperation across Iraq's oil, gas and electricity sectors. Planned talks include projects to capture associated gas, increase power generation, expand energy storage capacity...

Chinese crude oil imports this month are on course to book an even weaker month than May, according to Kpler data, which sees the daily average at just 6.4 million barrels, as cited by Bloomberg. Data from Vortexa suggests a similar daily import level, the publication added. This would be the weakest import rate since October 2016, Bloomberg noted, and an 8% decline on May volumes. Those averaged 7.82 million barrels, according to customs data, down by 29% on the year and 17% on April. The May...

Crude Oil prices edge lower on Friday, with the US benchmark West Texas Intermediate (WTI) barrel changing hands at $69.65 at the time of writing. This is the lowest price since February 27, one day before the US and Israel launched a joint attack on Iran.

West Texas Intermediate (WTI) US Oil trades around $69.30 at the time of writing, down 0.65% on Thursday. The American benchmark Crude is now posting a fourth consecutive day of losses, weighed down by a convergence of supply-side factors reshaping market expectations.

In the latest sign of recovering oil flows in the Persian Gulf, Qatar inked a deal with a Taiwanese refiner for the sale of a cargo of Al-Shaheen crude, Bloomberg reported today, citing unnamed trading sources. The deal follows the sale of Marine and Land Qatari crude to an Indian refiner last week, the sources also told the publication. Bloomberg also reported that ship-tracking data showed a Gfreek-owned supertanker currently loading at the Al-Shaheen floating storage terminal. Separately,...

Saudi Arabia is expected to slash the official selling prices of its crude loading for Asia in August, as Middle East’s crude benchmarks crashed amid the tentative reopening of the Strait of Hormuz and the oil supply increase from the region. Saudi oil giant Aramco, the world’s single-biggest crude oil exporter, is expected to slash the OSP of its flagship Arab Light crude by between $6.50 and $8.00 per barrel, a of industry sources showed on Friday. Refiners polled by Reuters...

ADNOC, the national oil company of Abu Dhabi, has cut the official selling price for July for its flagship Murban crude to $101.48 per barrel, down from $104.44 a barrel for June, amid weakening international and Middle Eastern benchmark oil prices. ADNOC’s recent pricing list for July, reported by Economy Middle East, reflects softening market conditions following the tentative reopening of the Strait of Hormuz. ADNOC has priced its other grades, Umm Lulu, Das, and Upper Zakum, at par with...

India’s economy could return to the trajectory to grow by 7% and even more in the fiscal year through March 2027 if oil prices remain close to the current $70 per barrel, according to a senior official at India’s central bank. Oil prices at about $70 a barrel eased tensions in the Middle East, and a pick-up in tanker traffic at the Strait of Hormuz would reduce upward pressure on India’s inflation and improve the outlook for its economy, Nagesh Kumar, an external member of the Reserve Bank of...

Natural gas markets are on course to return to balance in the third quarter of the year as the Strait of Hormuz reopens, the head of the Gas Exporting Countries Forum has said. “If we assume that the Strait (of Hormuz) is now open and will remain open, our view is actually that in the course of this next quarter we will begin to see some re-stabilization in the market,” Philip Mshelbila said at the Reuters Global Energy Forum, as quoted by the publication. The GECF groups producer countries...